As we move into the first quarter of 2026, the economic conversation in Canada has shifted from “temporary spikes” to “persistent pressures.” For investors, inflation-proofing portfolio Canada 2026 is no longer a niche strategy—it is a survival requirement. While the extreme volatility of previous years has subsided, the “new normal” of 2.4% inflation means that the purchasing power of your savings is under constant attack. Without a proactive approach to protecting purchasing power in Canada, a static portfolio will effectively lose value every single month.

The landscape of inflation-proofing portfolio Canada 2026 is heavily influenced by the Bank of Canada’s recent decisions. With the policy rate held at 2.25% as of January 28, 2026, the era of “easy money” is over, and the era of “real returns” has begun. In this environment, Wealth Management in Canada must focus on assets that have a direct correlation with rising costs. Whether you are a retiree concerned about fixed income or a business owner protecting corporate surplus, understanding the mechanics of inflation is the first step toward resilience.

Choosing the best inflation hedge investments requires looking beyond traditional GICs or savings accounts. While a 3.5% GIC might seem safe, after accounting for 2.4% inflation and marginal tax rates, your real return is often negative. This is why inflation-proofing portfolio Canada 2026 emphasizes assets with “pricing power”—companies and instruments that can pass on costs to the consumer. This article serves as the definitive guide to navigating these challenges, integrating Investment Planning in Canada with the latest 2026 economic data.

Ultimately, protecting purchasing power in Canada is about maintaining your standard of living. In cities like Toronto and Vancouver, where the cost of services and shelter remains high, a standard balanced fund may not be enough. By the end of this 4,000-word analysis, you will have a clear blueprint for inflation-proofing portfolio Canada 2026, ensuring that your wealth grows in real terms, not just nominal ones.

Table of Contents

The Bank of Canada’s 2026 Outlook: Interest Rates and CPI Impact

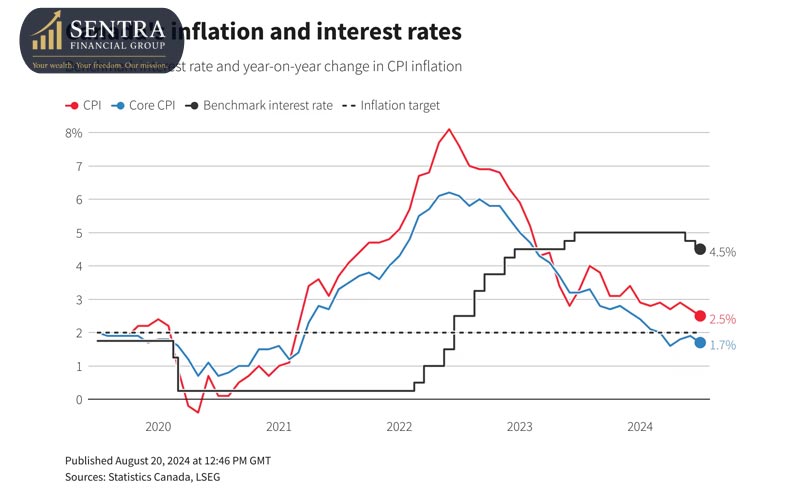

The most significant factor in inflation-proofing portfolio Canada 2026 is the stance of our central bank. On January 28, 2026, the Bank of Canada maintained the overnight rate at 2.25%. Governor Tiff Macklem noted that while inflation is nearing the 2% target, structural adjustments—including US trade tariffs and shifting demographics—mean that the BoC must remain vigilant. For investors, this “steady hand” means that interest-rate-sensitive assets are finally finding a floor.

Understanding the 2.4% Inflation Reality

In early 2026, the Consumer Price Index (CPI) reflects a complex mix of cooling energy prices and rising service costs. For those focused on inflation-proofing portfolio Canada 2026, the “headline” number of 2.4% only tells half the story. Core inflation measures, which strip out volatile items, are still hovering around 2.5%. This persistent core inflation is what eats away at long-term wealth, making Personal Financial Planning in Canada more critical than ever.

Interest Rates: The “Neutral” Zone

With Bank of Canada interest rates 2026 sitting at 2.25%, we are in what economists call the “neutral range.” This is neither stimulative nor restrictive. For your inflation-proofing portfolio Canada 2026 strategy, this means that fixed-income yields are high enough to be relevant but not high enough to compensate for high-tax environments. This balance necessitates a move toward more sophisticated hedges like real return bonds Canada and infrastructure-linked assets.

The US Trade Factor and the Loonie

A major headwind for protecting purchasing power in Canada in 2026 is the volatility of the Canadian dollar, currently trading near 72 cents USD. As a net importer of many consumer goods, a weak loonie fuels “imported inflation.” A robust inflation-proofing portfolio Canada 2026 should therefore include US-denominated assets or Canadian companies with significant US earnings, providing a natural currency hedge against a devaluing domestic dollar.

Real Estate vs. REITs: The 2026 Performance Breakdown

Real estate has historically been one of the best inflation hedge investments, but 2026 has brought a divergence between physical property and public markets. When considering Canadian REITs performance 2026, investors are finding that liquidity and diversification are often more valuable than direct ownership in a high-cost environment.

Physical Real Estate: High Barriers, High Costs

In 2026, the “shelter” component of the CPI remains a primary driver of inflation. While this benefits landlords who can raise rents, the rising costs of property taxes, insurance, and maintenance are cutting into net operating income (NOI). For those in Toronto, inflation-proofing portfolio Canada 2026 through physical rentals requires significant capital and management time, making it less efficient for many Wealth Management in Canada clients.

Canadian REITs Performance 2026: The Recovery Year

Publicly traded Real Estate Investment Trusts (REITs) are seeing a resurgence. As Bank of Canada interest rates 2026 have stabilized, the “cap rate expansion” that plagued REITs in 2024-2025 has slowed. Analysts are projecting mid-to-high single-digit returns for the sector this year. Canadian REITs performance 2026 is particularly strong in the industrial and grocery-anchored retail sectors, where leases are often indexed to inflation.

Adding REITs to your inflation-proofing portfolio Canada 2026 allows for a liquid, diversified exposure to real assets. Furthermore, because REIT dividends are often treated as a mix of income and return of capital, they can be highly tax-efficient when held in a non-registered account. This is a key tactic in Investment Strategies for the Affluent, providing a growing yield that outpaces the CPI.

The Power of Pricing Power: Stocks That Thrive When Prices Rise

In the context of inflation-proofing portfolio Canada 2026, not all equities are created equal. The most successful investors this year are focusing on companies with “Pricing Power”—the structural ability to raise prices without a significant drop in demand. In a 2.4% inflation environment, these firms act as a natural passthrough, protecting your real returns from being eroded by rising input costs.

Canadian Oligopolies: The Inflation-Proof Moat

Canada’s economy is defined by its strong oligopolies, which are the best inflation hedge investments for a conservative portfolio.

- The “Big Three” Telecoms: With the integration of major networks complete in early 2026, companies like Telus and Rogers have demonstrated immense pricing power. As seen in recent Wealth Management in Canada reports, these firms have successfully adjusted service fees to match the rising cost of infrastructure, maintaining robust margins.

- Class 1 Railroads: Canadian National Railway (CN) and Canadian Pacific Kansas City (CPKC) remain vital. As the “arteries” of the North American economy, they have fuel surcharge clauses and the ability to raise freight rates, making them a staple in any inflation-proofing portfolio Canada 2026.

Energy and Infrastructure: Visible Growth in 2026

Early 2026 has seen a resurgence in energy infrastructure. TC Energy (TSX:TRP) and Enbridge (TSX:ENB) are standout performers, offering yields between 5.2% and 5.4%. These companies operate under long-term, inflation-linked contracts. As part of our Investment Planning in Canada strategy, we highlight TRP’s expansion into nuclear power (Bruce Power), which provides a stable, low-commodity-risk cash flow that thrives even when other sectors struggle with rising prices.

Fixed Income Strategy: Real Return Bonds Canada (RRBs)

While traditional bonds often suffer when inflation surprises to the upside, real return bonds Canada are specifically engineered to solve this problem. As of February 2026, the long-term benchmark yield for RRBs sits at 1.84% plus the inflation adjustment. This makes them a “contractual” hedge that many Financial Planner and Retirement Specialists are now prioritizing.

How RRBs Protect Your Purchasing Power

Unlike standard Government of Canada bonds, the principal of an RRB is adjusted upward based on the Consumer Price Index (CPI). If inflation rises by 3%, your bond’s face value increases by 3%, and your semi-annual interest payment is calculated on this new, higher amount. This ensures that you are protecting purchasing power in Canada by locking in a “real” rate of return above the inflation rate.

The 2026 “Phantom Tax” Warning

A critical detail for inflation-proofing portfolio Canada 2026 is the taxation of RRBs. The CRA taxes the inflationary increase on the principal every year, even if you haven’t received that cash yet. To maintain the effectiveness of this hedge, it is vital to hold real return bonds Canada within a tax-sheltered account like a TFSA or RRSP. This prevents the “tax drag” from negating your inflation protection, a common topic in our RRSP vs. TFSA Withdrawal Strategy guides.

Dividend Stocks for Inflation: The 2026 “Kings”

When building an inflation-proofing portfolio Canada 2026, “yield” is not enough; you need “dividend growth.” Companies that can consistently grow their payouts faster than the 2.4% CPI are the true winners.

Top Performers of February 2026

- Natural Gas Leaders: Tourmaline Oil (TSX:TOU) has become a favorite for 2026 due to its ability to generate massive free cash flow and pay special dividends. With natural gas serving as a key transition fuel, TOU is well-positioned for both growth and income.

- Financial Strength: Power Corporation of Canada (TSX:POW) continues to be a top pick. Its diversified holdings in insurance and wealth management provide a steady stream of dividends that have historically outpaced inflation. As noted in Wealth Management in Canada, financial firms often benefit from the current 2.25% interest rate environment, which allows for healthier lending margins.

The Utility Shield: Emera and Fortis

For those seeking lower volatility, Emera (TSX:EMA) is targeting a 7-8% rate base growth through 2030. Because utilities are regulated, they are often allowed to pass on increased operating costs to consumers, making them one of the best inflation hedge investments for long-term Retirement Planning in Canada.

Gold and Commodities: The Tactical Edge in Inflation-Proofing Portfolio Canada 2026

When the “silent thief” of inflation persists, paper assets can sometimes falter. In early 2026, many Wealth Management in Canada specialists are recommending a tactical allocation to hard assets. Commodities, particularly gold and industrial metals, have historically shown a low correlation with traditional stocks and bonds, making them a vital component of an inflation-proofing portfolio Canada 2026.

Gold as the Ultimate Store of Value

In February 2026, gold has reached new heights, driven by geopolitical uncertainty and its status as a hedge against currency debasement. While it doesn’t pay a dividend, gold is often considered one of the best inflation hedge investments because its supply cannot be manipulated by central bank policies. For an Investment Planning in Canada strategy, we typically suggest a 5% to 10% allocation to gold through physical bullion or low-cost ETFs.

Copper and Industrial Metals: The Green Energy Factor

Beyond gold, “red gold” (copper) is proving to be a powerhouse in 2026. As Canada accelerates its transition to a green economy, the demand for copper, lithium, and nickel has skyrocketed. Companies like Teck Resources (TSX:TECK.B) are essential for inflation-proofing portfolio Canada 2026 because their product prices are globally set and naturally rise when inflation hits the manufacturing and energy sectors.

Tax-Efficiency: The Hidden Pillar of Protecting Purchasing Power Canada

A common mistake in inflation-proofing portfolio Canada 2026 is ignoring the impact of taxes. Inflation often pushes investors into higher tax brackets—a phenomenon known as “bracket creep.” To truly succeed in protecting purchasing power in Canada, you must maximize your real, after-tax returns.

Maximizing the 2026 TFSA and RRSP Limits

The most effective way to shield your inflation-proof assets is through registered accounts. With the cumulative TFSA room reaching $109,000 in 2026, it is the ideal place for high-yield dividend stocks for inflation and REITs. Since withdrawals are tax-free, they do not trigger OAS clawbacks, ensuring that your government benefits are preserved while you fight rising costs. This is a primary focus of our Personal Financial Planning in Canada consultations.

Capital Gains vs. Interest Income

In a world of 2.4% inflation, earning interest income in a non-registered account is a losing battle. Interest is taxed at your full marginal rate, whereas capital gains and Canadian dividends receive preferential tax treatment. For Business Owners in Canada, shifting from interest-bearing vehicles to growth-oriented equities with pricing power is essential for inflation-proofing portfolio Canada 2026.

Alternative Investments: Private Equity and Infrastructure

For affluent investors, the best inflation hedge investments often lie outside the public markets. Private infrastructure projects—such as toll roads, pipelines, and renewable energy farms—often have “inflation-linked revenue streams” built into their contracts.

As interest rates from the Bank of Canada interest rates 2026 have stabilized at 2.25%, the cost of financing for these large-scale projects has become more predictable. Investing in private infrastructure provides a steady, index-linked cash flow that is largely immune to the daily volatility of the TSX. This sophistication is what characterizes modern Wealth Management in Canada.

Retirement Planning in 2026: Protecting Purchasing Power in the Golden Years

For those currently in or nearing retirement, inflation-proofing portfolio Canada 2026 is not just about growth—it’s about cash flow sustainability. In February 2026, the federal government confirmed that Canada Pension Plan (CPP) and Old Age Security (OAS) payments have been indexed by 2.0% to reflect the previous year’s cost-of-living increases. However, with the actual “on-the-ground” inflation for seniors (specifically in healthcare and specialized services) often exceeding the headline CPI, relying solely on government indexing is a risky strategy.

The 2026 CPP and OAS Reality

As of January 2026, the maximum monthly CPP retirement benefit has risen to $1,760 for those starting at age 65, reflecting the ongoing CPP enhancement program. While this is a welcome increase, protecting purchasing power in Canada requires private savings to do the heavy lifting. In our Retirement Planning in Canada sessions, we emphasize that the “real” value of a fixed pension erodes by nearly 22% over a 10-year period even at a modest 2% inflation rate.

The Variable Spending Strategy

To effectively manage an inflation-proofing portfolio Canada 2026, many affluent retirees are adopting “guardrail” spending strategies. Instead of a flat 4% withdrawal rate, they adjust their spending based on the performance of their best inflation hedge investments. In years where REITs or commodity-linked stocks perform well, they take a higher distribution; in flatter years, they rely on their “cash wedge” or short-term laddered GICs. This dynamic approach is a cornerstone of modern Wealth Management in Canada.

2026 Checklist: Final Steps for Inflation-Proofing Portfolio Canada

To wrap up your 2026 strategy, use this tactical checklist to ensure no part of your wealth is left exposed to the “silent thief” of inflation:

- [ ] Audit Dividend Growth Rates: Ensure your dividend stocks for inflation are increasing their payouts by at least 3-5% annually. In 2026, look for companies like Emera or TC Energy that have regulated rate-base growth.

- [ ] Rebalance into Real Assets: Confirm that at least 15-20% of your portfolio is in “hard assets” like Canadian REITs performance 2026 leaders or infrastructure funds.

- [ ] Optimize TFSA for Inflation Hedges: With the cumulative limit now at $109,000, move your most tax-inefficient inflation hedges (like Real Return Bonds or high-yield REITs) into this tax-free bucket.

- [ ] Currency Diversification: Ensure a portion of your portfolio is in USD-denominated assets. With the CAD trading around 72 cents in February 2026, US exposure acts as a vital hedge against domestic “imported inflation.”

- [ ] Review Insurance Cash Values: As part of Life Insurance Wealth Preservation Canada 2026, check the dividend scale of your Whole Life policy. These often provide a stable, non-correlated return that tracks long-term inflation trends.

Frequently Asked Questions: Inflation-Proofing Portfolio Canada 2026

Will the Bank of Canada interest rates 2026 go lower than 2.25%?

Most analysts, including those at S&P Global, expect the BoC to hold steady at 2.25% throughout 2026 to ensure core inflation (currently 2.4%) fully settles at the 2% target.

What are the best inflation hedge investments for a corporate account?

For Business Owners in Canada, corporate-owned life insurance and “Class 1” dividend-paying stocks are ideal, as they provide growth without triggering the passive income tax grind.

How does the 2026 CPP enhancement affect my portfolio?

The enhancement means you’ll receive a higher base pension, but it also means your payroll deductions have increased. Your inflation-proofing portfolio Canada 2026 should account for this reduced net cash flow in your working years.

Are GICs still relevant with Bank of Canada interest rates 2026 at 2.25%?

GICs are useful for capital preservation but weak for protecting purchasing power in Canada. If you use them, choose “laddered” GICs to ensure you can reinvest as rates adjust.

Why are real return bonds Canada better than regular bonds right now?

Regular bonds have a fixed coupon that loses value as prices rise. Real return bonds Canada adjust their principal based on the CPI, ensuring your investment keeps pace with the actual cost of living.

How does a weak Loonie affect my inflation-proofing strategy?

A weak dollar makes imports more expensive, which is “inflationary.” Holding US-denominated assets provides a hedge, as your wealth increases in CAD terms when the Loonie drops.

Conclusion: Thriving in the 2026 Economy

Inflation-proofing your wealth in 2026 is a multi-dimensional challenge that requires more than just picking a few “hot” stocks. It requires a fundamental shift in how you view Wealth Management in Canada. By focusing on protecting purchasing power in Canada through a mix of real return bonds, Canadian REITs, and dividend-growing equities, you move from a defensive posture to one of growth.

The 2026 economic landscape—characterized by a 2.25% Bank of Canada rate and a 2.4% inflation reality—demands precision. Whether you are using Life Insurance Wealth Preservation Canada 2026 to protect your estate or building an inflation-proofing portfolio Canada 2026 for retirement, the goal is the same: ensuring that every dollar you’ve worked for continues to work just as hard for you.

At Sentra Financial Group, we specialize in navigating these complex waters. From Investment Planning in Canada to sophisticated tax-shielding strategies, we are dedicated to helping you stay ahead of the curve. Don’t let inflation dictate your future—take control of your real returns today.

At Sentra Financial Group, we believe financial success isn’t about luck — it’s about strategy, discipline, and trust. Our mission is to help individuals and families achieve peace of mind through smart investing, life insurance, and long-term financial planning.