Investment planning and strategies in Canada are not about predicting markets or chasing returns. They are about building a structured approach that aligns investment decisions with long-term financial goals, risk tolerance, and time horizon. Without a clear framework, investing often becomes reactive, inconsistent, and disconnected from broader financial objectives.

Many Canadians approach investing as a standalone activity, focusing on individual products or short-term performance. Over time, this approach can lead to fragmented portfolios, misaligned risk exposure, and unnecessary volatility. Investment planning and strategies in Canada provide a disciplined alternative by integrating investing into a comprehensive financial plan.

At its core, investment planning is about decision-making under uncertainty. Markets are unpredictable, but personal goals and timelines are not. A well-designed investment strategy focuses on what can be controlled—asset allocation, diversification, costs, and behavior—rather than attempting to forecast market movements.

In the Canadian context, investment planning must also account for registered accounts, tax efficiency, and regulatory considerations. These factors influence how portfolios are structured and how returns are realized over time. Coordinating investments within this environment is essential for long-term success.

Effective investment planning and strategies in Canada serve as a bridge between day-to-day financial decisions and long-term objectives such as retirement and wealth accumulation. When aligned properly, investing becomes a tool that supports broader financial stability rather than a source of stress or speculation.

Table of Contents

What Is Investment Planning in Canada?

Investment planning in Canada refers to the process of designing and managing an investment strategy that supports long-term financial goals within the Canadian financial system. Unlike ad hoc investing, investment planning emphasizes structure, consistency, and alignment with personal circumstances.

This process begins with understanding objectives. Whether the goal is retirement income, long-term wealth building, or capital preservation, investment planning and strategies in Canada ensure that portfolio decisions are guided by purpose rather than market noise. Clear objectives provide context for every investment choice.

Risk tolerance is another defining element. Investment planning in Canada evaluates how much risk an individual can realistically take, both financially and emotionally. Aligning portfolio risk with tolerance helps reduce the likelihood of reactive decisions during periods of market volatility.

Time horizon plays a critical role in shaping investment strategy. Short-term goals require different approaches than long-term objectives. Investment planning and strategies in Canada account for these differences by matching asset allocation to timelines rather than adopting a one-size-fits-all approach.

Investment planning also integrates closely with broader financial considerations. Decisions related to investing are most effective when aligned with cash flow, tax planning, and retirement objectives established through personal financial planning in Canada. This integration ensures that investing supports, rather than undermines, long-term strategy.

Why Investment Planning Matters for Canadian Investors

The importance of investment planning and strategies in Canada has increased as individuals take on greater responsibility for their financial outcomes. With fewer traditional pensions and greater reliance on personal savings, investment decisions now play a central role in long-term financial security.

Market volatility is one reason investment planning matters. Without a structured plan, investors are more likely to react emotionally to short-term market movements. Investment planning in Canada provides a disciplined framework that supports consistent decision-making even during periods of uncertainty.

Tax efficiency is another critical factor. Investment returns are influenced not only by market performance but also by how investments are taxed. Coordinating investments across registered and non-registered accounts can significantly affect after-tax outcomes, making tax-aware investment planning essential.

Investment planning also helps manage behavioral risk. Fear and overconfidence are common drivers of poor investment decisions. By establishing clear guidelines in advance, investment planning and strategies in Canada help reduce the impact of emotional biases on long-term outcomes.

Finally, investment planning matters because it connects investing to real-world goals. Rather than focusing solely on returns, a structured strategy ensures that investments support objectives such as retirement readiness, lifestyle flexibility, and long-term financial independence.

Core Principles of Investment Planning and Strategies in Canada

Effective investment planning and strategies in Canada are grounded in a set of core principles that guide decision-making over time. These principles provide consistency and help investors remain focused on long-term outcomes rather than short-term distractions.

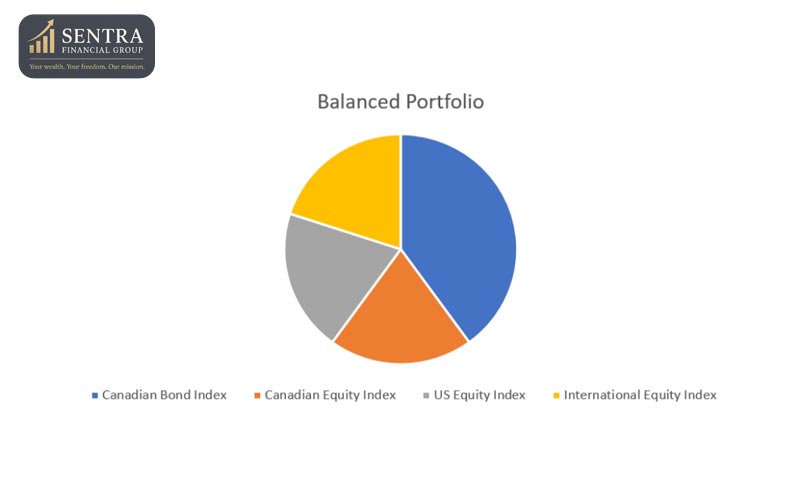

Asset allocation is one of the most important principles. The mix of asset classes within a portfolio largely determines risk and return characteristics. Investment planning in Canada emphasizes allocation decisions that align with goals, risk tolerance, and time horizon.

Diversification is closely related. Spreading investments across different asset classes, sectors, and regions helps reduce concentration risk. Investment planning and strategies in Canada use diversification to manage volatility rather than eliminate risk entirely.

Cost management is another essential principle. Investment fees and expenses compound over time and can significantly affect long-term returns. A disciplined investment planning approach considers costs as a controllable factor that influences outcomes.

Consistency and discipline complete the foundation. Investment planning in Canada prioritizes maintaining a long-term strategy through market cycles rather than making frequent changes based on short-term performance. This discipline supports more predictable outcomes over time.

Asset Allocation and Portfolio Structure in Canada

Asset allocation sits at the center of effective investment planning and strategies in Canada. It determines how risk and return are balanced across a portfolio and has a greater influence on long-term outcomes than individual security selection. Without a deliberate allocation framework, portfolios often drift toward unintended risk exposures.

In the Canadian context, asset allocation must reflect personal goals, time horizon, and tolerance for volatility. Short-term objectives require a different mix of assets than long-term wealth accumulation or retirement-focused strategies. Investment planning and strategies in Canada emphasize aligning allocation decisions with timelines rather than market forecasts.

Portfolio structure also matters. How assets are organized across accounts can affect risk management and tax efficiency. A well-structured portfolio coordinates holdings across registered and non-registered accounts so that each asset class is placed where it can perform most efficiently over time.

Rebalancing is an essential discipline within asset allocation. Market movements can gradually shift a portfolio away from its intended structure, increasing risk unintentionally. Investment planning and strategies in Canada incorporate systematic rebalancing to restore alignment without relying on emotional or reactive decisions.

Ultimately, asset allocation provides a framework for consistency. By defining allocation targets in advance, investors can maintain discipline through market cycles and ensure that portfolios remain aligned with long-term objectives rather than short-term noise.

Tax-Efficient Investing in the Canadian System

Tax efficiency is a defining feature of successful investment planning and strategies in Canada. Investment returns are meaningful only after taxes, and overlooking tax considerations can significantly reduce long-term outcomes. Coordinating investments within the Canadian tax system is therefore essential.

Canada offers a variety of registered accounts, each with distinct tax advantages. Using these accounts strategically allows investors to defer, reduce, or eliminate taxes on investment growth. Investment planning and strategies in Canada ensure that contributions and asset placement within these accounts support long-term efficiency rather than short-term convenience.

Non-registered accounts also play an important role, particularly for higher-income individuals and those with complex financial situations. Understanding how different types of investment income are taxed helps inform decisions about portfolio composition and withdrawal timing.

Tax efficiency extends beyond account selection. The type of investments held, the timing of transactions, and the realization of gains and losses all influence tax outcomes. Investment planning and strategies in Canada incorporate these considerations to manage tax exposure proactively rather than reactively.

Integrating tax-aware investing within a broader framework connected to personal financial planning in Canada helps ensure that tax efficiency supports overall financial goals rather than operating in isolation.

Investment Planning in Canada Across Life Stages

Investment planning and strategies in Canada evolve as individuals move through different stages of life. Financial priorities, risk tolerance, and timelines change over time, requiring investment strategies that adapt rather than remain static.

Early in life, investment planning often emphasizes growth. Longer time horizons allow for greater exposure to growth-oriented assets, and volatility can be managed through consistency and disciplined contributions. Investment planning and strategies in Canada help establish a foundation that supports long-term wealth accumulation.

Mid-life planning introduces new considerations. Increased income, family responsibilities, and competing financial priorities require more nuanced strategies. Investment planning during this stage focuses on balancing growth with stability while preparing for future objectives such as retirement.

As retirement approaches, investment planning shifts toward income sustainability and risk management. Portfolios are often adjusted to support predictable cash flow and reduce exposure to market volatility. Coordinating this transition with retirement planning in Canada helps ensure a smooth progression from accumulation to income generation.

Across all life stages, investment planning and strategies in Canada provide continuity. By maintaining a clear framework, investors can adapt to changing circumstances without undermining long-term objectives.

Common Investment Planning Mistakes Canadians Make

Many challenges in investing arise from avoidable mistakes rather than market conditions. One common error is treating investment decisions as isolated events rather than components of a broader strategy. Without investment planning and strategies in Canada, portfolios often become fragmented and inconsistent.

Another frequent mistake is chasing performance. Reacting to recent market trends can lead to buying high and selling low, undermining long-term results. Investment planning in Canada emphasizes discipline and long-term focus to counteract these behavioral tendencies.

Ignoring tax implications is also a common issue. Focusing solely on pre-tax returns can obscure the true impact of investment decisions. Investment planning and strategies in Canada incorporate tax considerations to support after-tax outcomes.

Many investors also fail to adjust strategies as circumstances change. Life events, income changes, and evolving goals require periodic review. Without regular reassessment, investment strategies may no longer align with objectives.

Finally, overconfidence or excessive conservatism can both hinder progress. Investment planning in Canada helps balance risk and opportunity by grounding decisions in analysis rather than emotion.

Working With an Investment Planning in Canada Professional

As investment complexity increases, many Canadians seek professional guidance to support investment planning and strategies in Canada. While basic investing can be done independently, comprehensive planning often benefits from experience and objectivity.

An investment planning professional helps translate goals into actionable strategy. By assessing risk tolerance, time horizon, and financial context, professionals design portfolios that align with long-term objectives rather than short-term market movements.

Objectivity is a key advantage of professional guidance. Market volatility and financial news can influence decision-making, often leading to reactive behavior. A structured planning approach provides discipline and consistency during uncertain periods.

Professional investment planning also emphasizes integration. Investing works best when coordinated with broader financial considerations such as retirement, tax planning, and cash flow. Aligning investment strategy with wealth management considerations supports cohesive long-term outcomes.

For many individuals, professional support provides confidence and accountability. Knowing that an investment strategy is monitored and adjusted as needed helps investors remain focused on long-term goals rather than short-term fluctuations.

Building a Disciplined Investment Strategy for the Long Term

Investment planning and strategies in Canada are ultimately about discipline and alignment. By focusing on asset allocation, tax efficiency, and long-term objectives, investors can navigate uncertainty with greater confidence and consistency.

A structured investment plan provides a clear framework for decision-making. It supports adaptability without sacrificing direction and helps investors remain committed to their goals through market cycles.

Integrating investment planning with broader financial strategy ensures that investing serves a purpose beyond returns alone. When aligned with retirement and personal financial planning, investment strategies become tools for long-term stability rather than sources of stress.

For those seeking clarity and structure, working within a disciplined framework supported by professional investment planning guidance can help transform complex investment decisions into a coherent and sustainable strategy.

Conclusion: Building a Disciplined Investment Planning in Canada

Investment planning and strategies in Canada are ultimately about discipline, alignment, and long-term clarity. Successful investing is rarely the result of predicting markets or identifying short-term opportunities. Instead, it comes from creating a structured framework that connects investment decisions to personal goals, risk tolerance, and time horizon.

A well-designed investment strategy provides direction during periods of uncertainty. Market cycles, economic changes, and emotional pressures are inevitable, but a clear plan helps investors remain focused on long-term objectives rather than reacting to short-term noise. This consistency plays a critical role in achieving sustainable outcomes over time.

Investment planning in Canada also emphasizes coordination. Asset allocation, tax efficiency, and portfolio structure must work together rather than in isolation. When investments are aligned with broader financial planning considerations, they become more effective tools for long-term wealth building and financial stability.

Another defining feature of effective investment planning is adaptability. While long-term goals remain relatively stable, financial circumstances and external conditions evolve. A structured investment plan allows for thoughtful adjustments without abandoning overall strategy, helping investors navigate change with confidence.

For Canadians seeking clarity and control over their financial future, investment planning and strategies in Canada provide a disciplined approach that transforms investing from a reactive activity into a purposeful component of long-term financial success.

At Sentra Financial Group, we believe financial success isn’t about luck — it’s about strategy, discipline, and trust. Our mission is to help individuals and families achieve peace of mind through smart investing, life insurance, and long-term financial planning.

FAQ About Investment Planning & Strategies in Canada

What is investment planning in Canada?

Investment planning in Canada is the process of designing and managing an investment strategy that aligns with long-term financial goals, risk tolerance, and time horizon within the Canadian financial system. It focuses on structure and consistency rather than short-term market predictions.

How are investment planning and investment strategies different?

Investment planning provides the overall framework, while investment strategies are the methods used within that framework. Planning defines objectives and constraints, and strategies implement those objectives through asset allocation, diversification, and portfolio management.

Why is investment planning important for Canadians?

Investment Planning in Canada is important because many Canadians rely on personal savings and investments for long-term goals such as retirement. Without a structured plan, investment decisions can become reactive and inconsistent, increasing risk and reducing long-term effectiveness.

Does investment planning in Canada include tax considerations?

Yes. Tax efficiency is a core component of investment planning in Canada. Coordinating registered and non-registered accounts, investment income types, and timing decisions can significantly influence after-tax returns over time.

Is investment planning only for long-term investors?

While long-term goals are a primary focus, investment planning in Canada is valuable for anyone with defined financial objectives. Even shorter-term goals benefit from structured planning that aligns risk and return expectations.

How often should an investment plan be reviewed?

An investment plan should be reviewed regularly and whenever significant changes occur, such as shifts in income, goals, or market conditions. Regular review helps ensure that strategies remain aligned with objectives.

How does investment planning connect to retirement planning?

Investment Planning in Canada supports retirement planning by aligning portfolio structure and risk management with future income needs. Coordinating these elements helps create a smoother transition from wealth accumulation to income generation later in life.