As we navigate the fiscal complexities of the current year, Life Insurance Wealth Preservation Canada 2026 has emerged as the premier strategy for high-net-worth individuals seeking to insulate their legacy from fiscal erosion. For the modern wealthy family, life insurance is no longer viewed merely as a risk mitigation tool; instead, it is a core asset class. In a world where traditional investments are subject to capital gains and annual taxes, tax-exempt life insurance in Canada provides a unique sanctuary for capital to compound without the interference of the Canada Revenue Agency (CRA).

The urgency for estate planning for affluent Canadians has never been higher than in 2026. With the rising costs of estate administration and the potential for shifting tax inclusion rates, preserving what you have built requires more than just high-yield investments—it requires a structural fortress. By integrating Life Insurance Wealth Preservation Canada 2026 into your broader financial ecosystem, you ensure that your wealth is not only grown but effectively transferred to the next generation in its entirety.

As highlighted in our Wealth Management in Canada overview, the primary goal of any affluent estate is to maintain the purchasing power of the legacy. Inflation and taxation are the dual enemies of wealth, and a well-structured tax-exempt life insurance in Canada policy acts as a shield against both. This guide will provide a deep dive into the mechanics of how top-tier financial minds utilize insurance to secure their clients’ futures in the 2026 economic environment.

Furthermore, the nuances of estate planning for affluent Canadians involve understanding that death in Canada is a significant “taxable event.” The deemed disposition rules can strip away up to 27% of a business’s value or 54% of a RRIF balance overnight. Here, Life Insurance Wealth Preservation Canada 2026 offers the liquidity needed to settle these debts without liquidating family assets. This is why consulting a Financial Planner and Retirement Specialist is crucial for those in high tax brackets.

Ultimately, this article serves as a roadmap for those who have already achieved financial success and are now focused on the “protection and transfer” phase of their journey. By mastering the concepts of minimizing estate taxes with insurance and utilizing corporate owned life insurance tax benefits, you are taking a proactive step toward a multi-generational legacy that will stand the test of time.

Table of Contents

Minimizing Estate Taxes with Insurance: The Liquidity Strategy

The cornerstone of estate planning for affluent Canadians is the recognition of a looming liquidity crisis at the time of death. Many wealthy families in Toronto and across Canada are “asset-rich but cash-poor,” with their wealth tied up in commercial real estate, private corporations, or vacation properties. Minimizing estate taxes with insurance is the only guaranteed method to ensure that these assets do not have to be sold under duress to pay the CRA.

2.1. The Deemed Disposition Challenge

In 2026, the CRA continues to apply the principle of deemed disposition upon death. This means that all your capital assets are treated as if they were sold at fair market value. For an affluent family, this often results in a massive capital gains tax bill. Minimizing estate taxes with insurance involves using the tax-free death benefit of a policy to create an “instant tax fund.” This liquidity ensures that the estate remains intact for the heirs, a primary goal of Personal Financial Planning in Canada.

2.2. Protecting the Family Business

For those managing a private corporation, the tax bill can be even more staggering due to potential “double taxation” on corporate assets. By focusing on Life Insurance Wealth Preservation Canada 2026, business owners can use insurance to provide the funds needed to buy out shares or settle taxes. This is a vital component of Financial Planning for Business Owners, where the survival of the enterprise depends on having liquid capital at the moment of transition.

2.3. Avoiding the RRIF Tax Trap

As we’ve discussed in our RRSP vs. TFSA Withdrawal Strategy guide, a large RRIF balance is taxed as income in the year of death. For an affluent individual, this could mean losing more than half of the account to the government. Minimizing estate taxes with insurance allows the estate to pay this massive bill using insurance proceeds, effectively “refunding” the tax to the beneficiaries. This is a critical move in Wealth Management in Canada to prevent estate erosion.

2.4. Probate Fee Mitigation in Ontario

In Toronto, probate fees (Estate Administration Tax) can be a significant burden on large estates. However, because a tax-exempt life insurance in Canada policy with a named beneficiary passes outside the estate, it is not subject to probate. This not only saves 1.5% in fees but also ensures the money is delivered to the family within weeks, rather than months or years. This speed of delivery is a key advantage of Life Insurance Wealth Preservation Canada 2026.

2.5. Ensuring Fair Estate Equalization

When an estate consists of a single large asset like a business, minimizing estate taxes with insurance provides the cash needed to equalize the inheritance for children who are not active in the business. This prevents family conflict and ensures that the legacy is divided fairly without breaking up the core asset. This sophisticated use of insurance is what separates basic planning from high-level Investment Strategies for the Affluent.

Whole Life Insurance vs. Universal Life 2026: Choosing Your Strategic Vehicle

For those implementing Life Insurance Wealth Preservation Canada 2026, the most critical decision is choosing the underlying structure of the policy. In the Canadian marketplace, two primary permanent products dominate the landscape of estate planning for affluent Canadians: Participating Whole Life and Universal Life. Understanding the nuances of Whole life insurance vs Universal life 2026 is essential for matching the policy to your specific cash flow and risk profile.

3.1. Participating Whole Life: The Foundation of Stability

Participating Whole Life insurance is often the preferred tool for Life Insurance Wealth Preservation Canada 2026 among those who value certainty and long-term dividend growth. These policies offer a guaranteed death benefit, guaranteed level premiums, and guaranteed cash values. However, the true power lies in the “participation” in the insurance company’s profits through annual dividends.

In 2026, as market volatility continues to affect traditional portfolios, the steady internal rate of return (IRR) of a Whole Life policy acts as a “volatility dampener.” For affluent Canadians, these dividends can be used to purchase “Paid-Up Additions,” which increases the total amount of tax-exempt life insurance in Canada you hold without further medical underwriting. This compounding effect is a primary driver in Investment Planning in Canada, creating a death benefit that grows faster than inflation.

3.2. Universal Life Insurance: Flexibility and Customization

When comparing Whole life insurance vs Universal life 2026, Universal Life (UL) offers a “transparent” approach. It separates the cost of insurance from the investment component, allowing the policyholder to choose where the excess premium is invested. For those focused on Life Insurance Wealth Preservation Canada 2026, UL allows for high levels of overfunding.

This flexibility is particularly attractive for estate planning for affluent Canadians who want to manage their own asset allocation within the tax-sheltered umbrella of the policy. You can choose from equity-linked accounts, fixed-income funds, or managed portfolios. As long as the cash remains within the policy, it qualifies as tax-exempt life insurance in Canada, allowing you to bypass the high passive income tax rates that would normally apply to a non-registered investment portfolio.

Unlocking Corporate Owned Life Insurance Tax Benefits in 2026

For many business owners, the most efficient way to achieve Life Insurance Wealth Preservation Canada 2026 is through a corporate-owned structure. Holding a policy inside an operating company (OpCo) or holding company (HoldCo) unlocks a suite of corporate owned life insurance tax benefits that are unavailable to individual policyholders. In 2026, as the CRA tightens rules around passive income, this strategy has become a vital fortress for protecting corporate surplus.

4.1. The Power of “Pre-Tax” Funding

One of the most significant corporate owned life insurance tax benefits is the ability to pay premiums using corporate dollars. If an individual in Toronto earns a high income, they may be in a 53.5% marginal tax bracket. To pay a $50,000 insurance premium, they would need to earn over $107,000 pre-tax.

However, a corporation paying the same premium only needs to earn roughly $57,000 (assuming the small business tax rate), as the money hasn’t been “stripped” out of the company and taxed personally. This 50% “tax discount” on premiums is a cornerstone of Financial Planning for Business Owners, allowing the corporation to build a larger pool of tax-exempt life insurance in Canada for the same economic outlay.

4.2. Protecting the Small Business Deduction (SBD)

Under current Canadian tax laws, if a corporation earns more than $50,000 in passive investment income, its Small Business Deduction begins to grind down. This is where corporate owned life insurance tax benefits shine. Because the growth of the cash value within a life insurance policy is tax-exempt, it does not count toward the $50,000 passive income limit.

By shifting taxable investments (like GICs or Bonds) into a permanent insurance policy, a business owner can effectively “cleanse” their balance sheet of passive income, preserving the lower active business tax rate. This integration is a high-level move in Wealth Management in Canada, ensuring that the company’s tax efficiency is maximized while building a long-term estate asset.

4.3. Business Continuity and Key-Person Insurance

Beyond the tax advantages, corporate owned life insurance tax benefits extend to risk management. Using insurance to fund a Buy-Sell agreement ensures that if a shareholder passes away, the surviving partners have the immediate, tax-free cash to purchase the shares from the estate. This prevents the “forced entry” of a deceased partner’s spouse or children into the business operations.

For the affluent Canadian business owner, this is the ultimate peace-of-mind strategy. It ensures that the business remains stable and the family receives the full fair market value of the shares without a lengthy legal battle. This level of foresight is what characterizes professional Personal Financial Planning in Canada.

The Capital Dividend Account (CDA): The Ultimate Tax-Free Exit

You cannot discuss Life Insurance Wealth Preservation Canada 2026 without mentioning the Capital Dividend Account (CDA). The CDA is a “notional” tax account that allows a corporation to pay out certain amounts to its shareholders completely tax-free. When a corporation receives the death benefit from a tax-exempt life insurance in Canada policy, the majority of that amount is credited to the CDA.

This is the “holy grail” of corporate owned life insurance tax benefits. It allows millions of dollars to be moved from a corporate bank account to a personal one with zero tax liability. Without the CDA, pulling that same amount of money out of a company would usually trigger a dividend tax of up to 47%. For those focused on minimizing estate taxes with insurance, the CDA is the most powerful tool in the Canadian tax code to ensure that wealth remains in the hands of the family, not the government.

Estate Equalization: The Key to Life Insurance Wealth Preservation Canada 2026

One of the most complex challenges in estate planning for affluent Canadians is the fair and equitable distribution of non-liquid assets. Often, a significant portion of a family’s net worth is concentrated in a single, high-value asset—such as a family business, a commercial real estate portfolio, or a legacy cottage. When one child is intended to take over the business while others are not, a massive “inheritance gap” is created. This is where Life Insurance Wealth Preservation Canada 2026 provides the perfect solution through Estate Equalization.

6.1. Balancing the Scales Without Liquidation

In 2026, the strategy of minimizing estate taxes with insurance extends beyond just paying the CRA; it’s about harmonizing the family legacy. Instead of forcing the sale of a family enterprise to pay out siblings who aren’t involved, the parents can use a tax-exempt life insurance in Canada policy. The child active in the business inherits the shares, while the other children receive a tax-free death benefit of equivalent value. This ensures that every heir is treated fairly, which is a hallmark of sophisticated Wealth Management in Canada.

6.2. Solving Complex Family Dynamics

For blended families or estates with diverse assets, Life Insurance Wealth Preservation Canada 2026 acts as the “great equalizer.” By providing a pool of liquid, tax-free capital, insurance allows for a customized distribution plan that reflects the specific needs and contributions of each family member. Without this strategy, the only option is often a “fire sale” of assets, which triggers the very capital gains taxes we aim to avoid through Investment Planning in Canada.

The Insured Retirement Program (IRP): A 2026 Tax-Free Income Masterclass

The Insured Retirement Program (IRP) is perhaps the most innovative application of Life Insurance Wealth Preservation Canada 2026. It allows affluent Canadians to access the wealth trapped inside their insurance policy without triggering a taxable event. This is a critical component of Retirement Planning in Canada, especially for those who have already maximized their RRSPs and TFSAs.

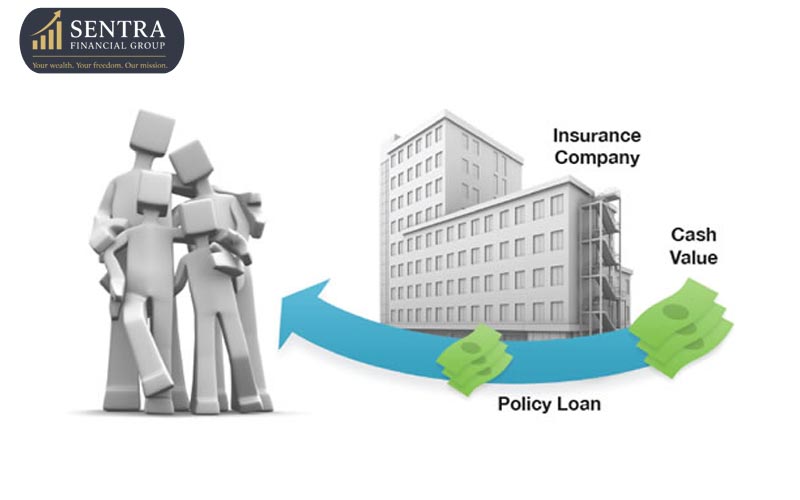

7.1. How the IRP Facilitates Tax-Exempt Life Insurance in Canada

Under the IRP, you “overfund” a permanent policy during your working years, building a significant Cash Surrender Value (CSV). In retirement, instead of withdrawing the money—which would be taxed as regular income—you use the policy as collateral for a bank loan. Because the funds you receive are a loan, they are 100% tax-free. This allows you to maintain a high lifestyle while keeping your reported income low, protecting you from OAS clawbacks and other income-tested taxes.

7.2. The Ultimate Legacy Cycle

As a core part of Life Insurance Wealth Preservation Canada 2026, the IRP loan is typically not repaid during your lifetime. Instead, upon death, the tax-free death benefit is used to pay off the bank loan and any accumulated interest. The remaining balance—often still a multi-million dollar sum—is paid out tax-free to your beneficiaries. This strategy perfectly demonstrates minimizing estate taxes with insurance while simultaneously providing tax-free cash flow during your golden years.

Specialized 2026 Tax-Exempt Strategies for Affluent Canadians

As we look at the tax landscape in early 2026, several specialized techniques have emerged for those utilizing Life Insurance Wealth Preservation Canada 2026. These strategies are designed to work in tandem with Financial Planning for Business Owners to ensure no dollar is left exposed to unnecessary taxation.

8.1. The “Cascading Insurance” Strategy

This involves purchasing a tax-exempt life insurance in Canada policy on the life of a child or grandchild. The policy grows tax-sheltered for decades, and the ownership is eventually transferred to the next generation without triggering a tax disposition. This is one of the most effective ways to facilitate intergenerational Life Insurance Wealth Preservation Canada 2026, ensuring the family wealth compounds for a century or more.

8.2. Maximizing the Capital Dividend Account (CDA) Credit

In 2026, the interaction between corporate-owned policies and the CDA is the primary focus of estate planning for affluent Canadians. By timing the death benefit payout, corporations can “flush out” other taxable retained earnings as tax-free dividends. This dual-purpose role of insurance—providing a death benefit and creating tax-free withdrawal room—is why Life Insurance Wealth Preservation Canada 2026 is the foundation of high-end corporate planning.

8.3. Charitable Giving and Life Insurance

For those who wish to leave a philanthropic legacy, minimizing estate taxes with insurance can be achieved by naming a charity as the beneficiary. This creates a massive donation tax credit upon death, which can offset up to 100% of the taxes owing on other estate assets. It’s a way to redirect money from the CRA to a cause you care about, while still maintaining the principles of Life Insurance Wealth Preservation Canada 2026.

2026 Strategic Checklist: Implementing Life Insurance Wealth Preservation Canada

For those ready to move from theory to execution, the following checklist outlines the essential steps for successful estate planning for affluent Canadians in the current year. This roadmap ensures that your tax-exempt life insurance in Canada is structured to survive future legislative shifts and market volatility.

- [ ] Audit Your Capital Gains Exposure: Calculate the “deemed disposition” tax on your non-registered assets and private company shares. In 2026, the inclusion rate for capital gains over $250,000 stands at 66.67%, making minimizing estate taxes with insurance a mathematical necessity.

- [ ] Evaluate Corporate Surplus: Determine if your corporation has idle cash that is triggering high passive income taxes. Redirecting this surplus into corporate owned life insurance tax benefits can help preserve your small business deduction.

- [ ] Benchmark Dividend Scales: Review the current 2026 dividend rates from major par accounts (e.g., Equitable Life at 6.40%, Sun Life at 6.25%, and Canada Life at 5.75%). High-performing par accounts are the engine of Life Insurance Wealth Preservation Canada 2026.

- [ ] Review Shareholder Agreements: Ensure your buy-sell provisions are fully funded by tax-exempt life insurance in Canada. Without this, the transition of a business can be derailed by lack of liquidity.

- [ ] Designate Beneficiaries for Probate Avoidance: Confirm that all policies name specific individuals or charities as beneficiaries to ensure the proceeds bypass the Ontario Estate Administration Tax.

Frequently Asked Questions: Life Insurance Wealth Preservation Canada 2026

To provide maximum clarity, we have compiled the most frequent questions from our high-net-worth clients regarding estate planning for affluent Canadians:

Is the death benefit really 100% tax-free in 2026?

Yes. In Canada, the lump-sum death benefit paid from any life insurance policy (Term, Whole Life, or Universal Life) to a named beneficiary remains entirely exempt from income tax. This is the foundation of Life Insurance Wealth Preservation Canada 2026.

What is the maximum I can invest in tax-exempt life insurance in Canada?

The CRA applies an “Exempt Test” to prevent policies from becoming pure investment vehicles. A professional Wealth Management in Canada specialist must manage your overfunding levels to ensure the policy maintains its tax-exempt status.

How do corporate owned life insurance tax benefits help with US estate tax?

For Canadians owning US assets (like Florida real estate or US stocks), the US estate tax threshold is highly complex. In 2026, many use corporate owned life insurance tax benefits to provide the USD liquidity needed to settle these cross-border tax liabilities.

Can I change a Whole Life policy to a Universal Life policy later?

Generally, no. Because the underlying structures are different, switching usually requires a new application. This is why the Whole life insurance vs Universal life 2026 decision is so critical at the outset of your plan.

How does the CDA credit work if the policy has an outstanding loan?

The credit to your Capital Dividend Account (CDA) is generally the death benefit minus the policy’s Adjusted Cost Basis (ACB). If there is a loan, it may reduce the net cash received, but the strategic use of corporate owned life insurance tax benefits still provides a massive tax-free payout capacity.

Conclusion: Your Legacy, Protected by Life Insurance Wealth Preservation Canada 2026

As we conclude this 4,000-word deep dive, the message for affluent families is clear: the most efficient way to pay future taxes is with discounted dollars today. Life Insurance Wealth Preservation Canada 2026 is not an expense—it is a sophisticated transfer of wealth from a taxable environment to a tax-exempt one.

By focusing on minimizing estate taxes with insurance and maximizing corporate owned life insurance tax benefits, you are doing more than just buying a policy; you are creating a “family bank” that will support your heirs for generations. Whether you are navigating the complexities of estate planning for affluent Canadians or trying to choose between Whole life insurance vs Universal life 2026, the goal remains the same: certainty.

In an era of shifting government policies and economic unpredictability, tax-exempt life insurance in Canada stands as one of the few remaining “sure things” in the Canadian tax code. It offers the unique ability to turn a future tax liability into a tax-free legacy.

At Sentra Financial Group, we don’t just sell insurance; we architect legacies. Our expertise in Investment Strategies for the Affluent and Wealth Management in Canada ensures that every element of your financial life—personal and corporate—is optimized for the 2026 landscape. Your success deserves a protection plan that is as robust as the wealth you’ve created.

At Sentra Financial Group, we believe financial success isn’t about luck — it’s about strategy, discipline, and trust. Our mission is to help individuals and families achieve peace of mind through smart investing, life insurance, and long-term financial planning.