Retirement planning in Canada is no longer a simple calculation based on age and savings. It has become a long-term strategic process that requires careful coordination of income sources, tax considerations, investment decisions, and lifestyle expectations. As life expectancy increases and traditional pension structures evolve, Canadians are facing more responsibility than ever when it comes to securing their financial future.

For many individuals, retirement can span twenty to thirty years or more. During this time, financial decisions made early in retirement can have a lasting impact on income stability, tax exposure, and overall quality of life. Without a structured plan, even individuals with substantial savings may experience uncertainty, stress, or unintended financial shortfalls later in life.

Retirement planning provides a framework for understanding how financial resources will be used over time. Rather than focusing solely on how much money has been saved, effective planning addresses how income will be generated, how risks will be managed, and how financial flexibility can be maintained throughout different stages of retirement.

In the Canadian context, retirement planning also requires navigating government programs, registered accounts, and a progressive tax system. These elements introduce opportunities but also complexity, making a coordinated approach essential. Retirement planning is therefore not a one-time decision, but an ongoing process that evolves as personal circumstances, markets, and regulations change.

A comprehensive retirement plan helps transform uncertainty into clarity. It allows individuals and families to make informed decisions with confidence, knowing their financial strategy is aligned with their long-term goals and realities.

Table of Contents

What Is Retirement Planning in Canada?

Retirement planning in Canada refers to the process of organizing financial resources in a way that supports income needs after employment income ends. Unlike basic saving strategies, retirement planning focuses on how assets are converted into sustainable income while managing taxes, risks, and long-term financial obligations.

At its core, retirement planning in Canada integrates multiple components of an individual’s financial life. These include personal savings, investments, employer-sponsored pensions, and government benefits. Each element plays a different role, and their interaction determines whether retirement income will remain stable over time.

One of the defining characteristics of retirement planning is its emphasis on longevity. Because no one can predict exactly how long retirement will last, plans must be designed to accommodate a wide range of possible outcomes. This requires balancing growth and preservation while maintaining enough flexibility to adapt to changing conditions.

In Canada, retirement planning is further shaped by specific rules governing registered accounts such as RRSPs and TFSAs, as well as programs like CPP and OAS. Decisions about when and how to use these resources can significantly affect long-term income and tax efficiency. These decisions are rarely optimal when made in isolation.

As part of a broader financial strategy, retirement planning in Canada connects closely with personal financial planning in Canada. While personal financial planning addresses overall goals and cash flow, retirement planning focuses on ensuring those goals remain achievable throughout the later stages of life.

Why Retirement Planning Matters More Than Ever

The importance of retirement planning has increased significantly over the past several decades. Changes in employment patterns, rising living costs, and longer life expectancy have shifted more responsibility onto individuals to manage their own retirement outcomes.

One of the most significant challenges facing retirees today is longevity risk. Living longer is a positive outcome, but it also means retirement savings must last longer than in previous generations. Without proper planning, individuals risk depleting their resources prematurely or being forced to reduce their standard of living later in life.

Inflation is another critical factor that makes retirement planning in Canada essential. Even moderate inflation can erode purchasing power over time, particularly for retirees on fixed incomes. Planning for inflation helps ensure that income remains sufficient not just at the start of retirement, but throughout its duration.

Market volatility adds another layer of complexity. The early years of retirement are particularly sensitive to investment performance, as withdrawals combined with poor market returns can permanently reduce portfolio longevity. A structured retirement plan accounts for this risk and aligns investment decisions with income needs.

Tax considerations further reinforce the need for proactive retirement planning in Canada. Canada’s progressive tax system means that unplanned withdrawals can lead to higher tax rates and reduced government benefits. Coordinating income sources and timing withdrawals strategically can significantly improve long-term outcomes and support a more stable retirement.

Key Components of Retirement Planning in Canada

Effective retirement planning is built on a combination of interconnected components that must work together cohesively. Focusing on only one aspect, such as investment growth, without considering income sustainability or tax efficiency often leads to suboptimal results.

Retirement income planning is one of the most important components. This involves determining how much income is needed to support a desired lifestyle and identifying reliable sources to meet that need. Income planning shifts the focus from asset accumulation to cash flow sustainability.

Investment strategy remains a key element, but its role evolves in retirement. Rather than prioritizing aggressive growth, investments must support income generation while managing volatility. This requires aligning portfolio structure with risk tolerance, time horizon, and withdrawal needs, often in coordination with investment planning in Canada.

Tax planning plays a critical role in preserving retirement income. Different income sources are taxed differently, and the sequence of withdrawals can affect lifetime tax exposure. Thoughtful tax planning helps retirees keep more of what they have saved while maintaining eligibility for income-tested benefits.

Risk management is another essential component. Health-related expenses, unexpected costs, and market downturns can all disrupt retirement plans. A comprehensive approach anticipates these risks and incorporates contingency planning to maintain financial resilience.

Together, these components form the foundation of a structured retirement strategy. When integrated properly, they support long-term stability and align retirement outcomes with personal goals and priorities.

Understanding Retirement Income Sources in Canada

Understanding where retirement income comes from is a foundational step in building a reliable retirement plan. In Canada, retirement income is rarely derived from a single source. Instead, it is typically a combination of personal savings, employer-sponsored plans, and government benefits, each with distinct characteristics that influence how and when income is received.

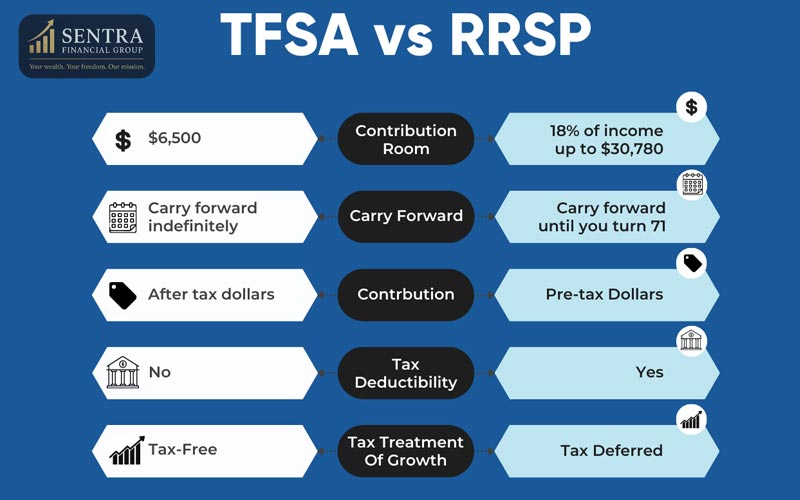

Personal savings often represent the most flexible component of retirement income. Accounts such as RRSPs, TFSAs, and non-registered investments allow individuals to control the timing and amount of withdrawals. However, this flexibility also introduces complexity, as each account type is taxed differently and serves a unique strategic purpose during retirement.

Employer-sponsored pension plans, when available, add another layer of income stability. Defined benefit pensions provide predictable lifetime income, while defined contribution plans depend on accumulated balances and investment performance. Integrating pension income with personal savings is critical to avoid over-reliance on a single income stream or inefficient withdrawal patterns.

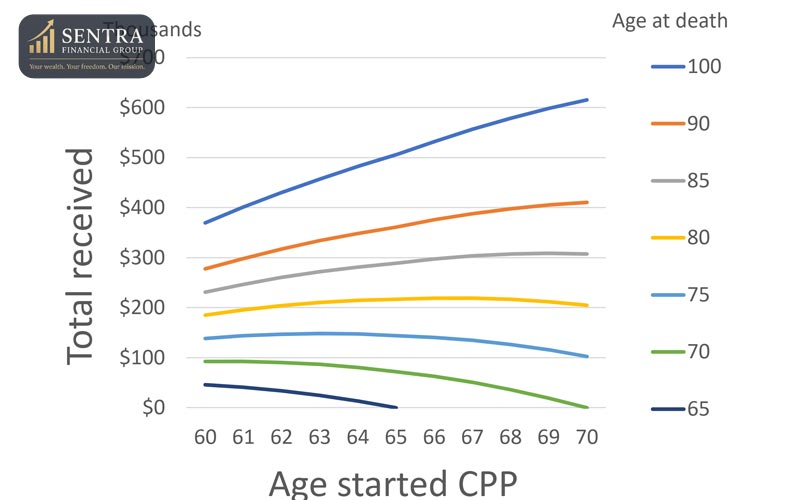

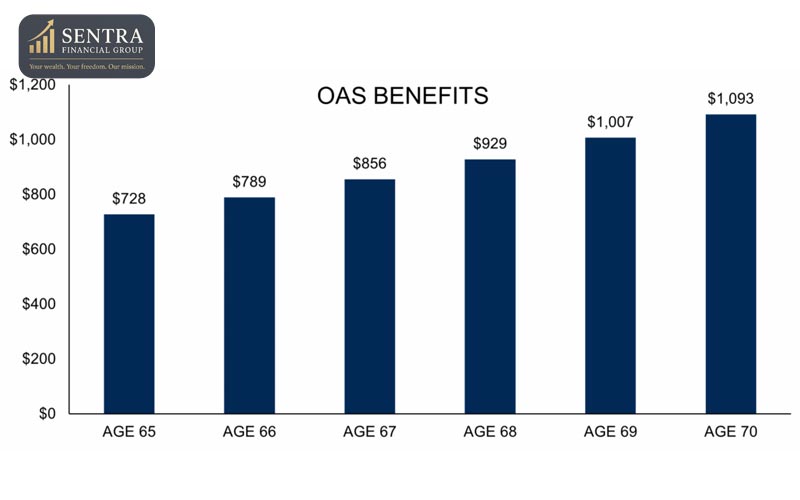

Government benefits, particularly the Canada Pension Plan (CPP) and Old Age Security (OAS), play a central role for most retirees. These benefits provide baseline income, but the timing of when they are claimed can significantly affect long-term financial outcomes. Claiming benefits too early may reduce lifetime income, while delaying them without proper planning can create short-term cash flow challenges.

Effective retirement planning in Canada focuses on coordinating these income sources rather than treating them independently. This coordination is a core element of structured retirement planning services, where the goal is to create a balanced and sustainable income stream that adapts over time rather than relying on static assumptions.

Retirement Withdrawal Strategies and Tax Efficiency

Withdrawal strategy is one of the most influential yet frequently overlooked aspects of retirement planning. The way funds are withdrawn can have a greater impact on long-term financial outcomes than investment returns alone. Poorly planned withdrawals often result in higher taxes, reduced government benefits, and unnecessary financial stress later in retirement.

In Canada, retirees typically withdraw income from a mix of registered and non-registered accounts. Each withdrawal decision triggers different tax consequences, and the order in which accounts are accessed plays a critical role in managing taxable income. Strategic sequencing of withdrawals can help smooth income over time and reduce exposure to higher marginal tax rates.

Tax efficiency becomes increasingly important as retirees begin drawing income from multiple sources. Large withdrawals from registered accounts can push individuals into higher tax brackets, while insufficient planning may result in the clawback of income-tested benefits such as OAS. A thoughtful withdrawal strategy seeks to balance current income needs with long-term tax optimization.

Another important consideration is the timing of withdrawals relative to market conditions. Withdrawing heavily during periods of market downturn can permanently reduce portfolio longevity. Retirement planning accounts for this risk by aligning withdrawal strategies with investment structure and cash reserves.

Because withdrawal decisions are ongoing rather than one-time events, they must be revisited regularly. Coordinated withdrawal planning works best when integrated with broader investment planning in Canada, ensuring that income needs and portfolio strategy remain aligned throughout retirement.

Common Retirement Planning Mistakes Canadians Make

Many retirement challenges stem not from a lack of savings, but from avoidable planning mistakes. One of the most common errors is assuming that retirement planning in Canada ends once retirement begins. In reality, retirement introduces a new phase of financial decision-making that requires ongoing attention and adjustment.

Another frequent mistake is underestimating the impact of taxes. Retirees often focus on gross income without considering how taxes reduce net cash flow. Without proactive planning, individuals may unintentionally increase their lifetime tax burden or lose access to government benefits designed to support retirees.

Overconfidence in investment performance is also a common issue. Relying on optimistic return assumptions can create a false sense of security and lead to unsustainable withdrawal rates. Market volatility, especially in the early years of retirement, can significantly alter long-term outcomes if not properly managed.

Many Canadians also delay important decisions such as CPP and OAS timing without understanding the long-term implications. These benefits are permanent choices, and claiming them without analysis can reduce total lifetime income. retirement planning in Canada helps evaluate these decisions within the context of the overall financial picture.

Finally, a lack of coordination between different aspects of financial planning often leads to inefficiencies. Retirement planning works best when it is integrated with personal financial planning in Canada, ensuring that retirement decisions support broader life goals rather than operating in isolation.

Retirement planning in Canada for Different Life Situations

Retirement planning is not a one-size-fits-all process. Different life stages and personal circumstances require different strategies, timelines, and priorities. Recognizing these differences is essential for creating a plan that remains relevant and effective over time.

For individuals approaching retirement, planning often focuses on transitioning from accumulation to income generation. This stage involves assessing readiness, refining investment strategy, and establishing clear withdrawal plans. Small adjustments made during this period can significantly improve long-term sustainability.

Those already in retirement face a different set of challenges. Managing income consistency, adapting to changing expenses, and responding to market conditions become central concerns. Ongoing planning helps retirees maintain flexibility and confidence as circumstances evolve.

Business owners require special consideration within retirement planning in Canada. Their wealth is often tied to the value of their business, making diversification and exit planning critical. Coordinating retirement strategy with business decisions helps reduce dependency on a single outcome and supports long-term security.

Life events such as health changes, family responsibilities, or shifts in lifestyle can also affect retirement plans. A structured approach allows adjustments without undermining overall stability. This adaptability is a defining feature of professional financial planning for business owners and individuals alike.

Ultimately, effective retirement planning in Canada reflects personal priorities and evolving circumstances. By accounting for different life situations, a retirement plan becomes a dynamic tool rather than a static projection.

Retirement Planning in Toronto vs Other Parts of Canada

Location plays a meaningful role in retirement planning, particularly in a country as geographically and economically diverse as Canada. While national programs and tax rules apply broadly, regional differences in cost of living and lifestyle can significantly influence retirement outcomes.

Toronto, for example, presents unique considerations due to higher housing costs and living expenses. Retirees in major urban centres often require higher income levels to maintain their desired lifestyle, making careful income planning especially important.

Tax considerations may also vary depending on provincial rates and local factors. Understanding how these differences affect net income is essential for accurate planning and realistic expectations. A national approach to retirement planning must be adaptable to regional realities.

Access to healthcare, transportation, and community resources can further influence retirement decisions. These factors may affect spending patterns and long-term planning assumptions, particularly for retirees considering relocation or downsizing.

For individuals specifically planning retirement in the Toronto area, localized insights can provide additional clarity. These considerations are explored in more detail within retirement planning in Toronto, which complements a broader national retirement strategy.

When Should You Start Retirement Planning?

One of the most common questions Canadians ask is when retirement planning should begin. Many assume that planning only becomes relevant a few years before retirement, but this perspective often limits available options and increases long-term risk. In reality, retirement planning in Canada is most effective when it begins well before retirement is imminent.

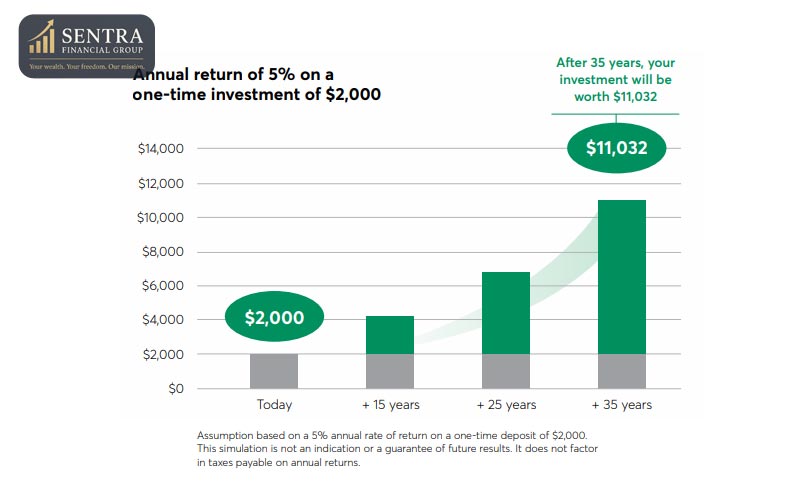

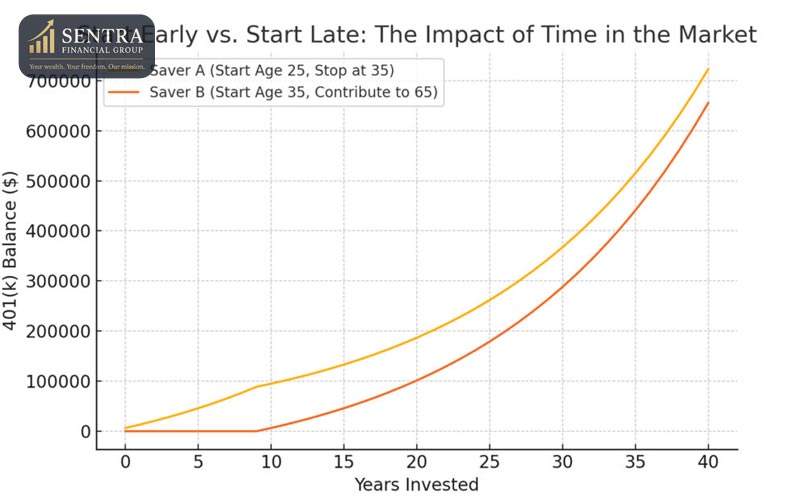

Starting early allows individuals to take advantage of time as a strategic asset. Longer time horizons provide greater flexibility in investment strategy, contribution planning, and tax efficiency. Early planning also reduces the pressure to make aggressive or reactive decisions later in life when options may be more limited.

That said, retirement planning in Canada remains valuable even for those who begin later. Individuals who start planning closer to retirement can still improve outcomes by optimizing withdrawal strategies, coordinating income sources, and managing tax exposure more effectively. While early planning offers more flexibility, late planning still offers meaningful opportunities for improvement.

Life events often serve as natural triggers for retirement planning. Career changes, business growth or exit considerations, family responsibilities, and health-related factors can all influence retirement priorities. A structured planning approach helps incorporate these changes without undermining long-term stability.

Ultimately, the best time to start retirement planning in Canada is when financial decisions begin to affect long-term outcomes. Working with a structured approach to professional retirement planning support helps ensure that timing decisions are aligned with personal goals rather than assumptions or external pressures.

Working With a Retirement Planning Professional

As retirement planning becomes more complex, many Canadians consider working with a professional to gain clarity and structure. While some financial decisions can be made independently, retirement planning in Canada often involves interconnected choices that benefit from experienced guidance.

A retirement planning professional helps translate financial information into actionable strategy. This includes evaluating income needs, coordinating savings and benefits, and identifying risks that may not be immediately apparent. Rather than focusing on isolated recommendations, a planning-based approach considers how decisions interact over time.

One of the key advantages of professional guidance is objectivity. Retirement decisions can be emotionally charged, particularly when markets are volatile or retirement is approaching. An experienced planner provides a disciplined framework that helps reduce reactive decision-making and supports long-term consistency.

Professional retirement planning also emphasizes integration. Retirement strategy does not exist in isolation but connects closely with broader financial goals, investment structure, and tax considerations. This integration ensures that retirement decisions reinforce rather than conflict with other aspects of financial planning.

For many individuals, working with a professional provides confidence and accountability. Structured guidance through a comprehensive personal financial planning approach helps ensure that retirement strategies remain aligned as circumstances evolve.

How Retirement Planning Fits Into Your Overall Financial Plan

Retirement planning is one component of a broader financial strategy, not a standalone exercise. Decisions related to retirement influence cash flow, investment structure, and long-term goals across every stage of life. Understanding this connection helps ensure that retirement planning supports, rather than restricts, overall financial flexibility.

Personal financial planning provides the foundation upon which retirement planning is built. Cash flow management, savings habits, and risk tolerance established earlier in life shape retirement readiness and income sustainability. retirement planning in Canada refines these elements with a long-term income focus.

Investment planning plays a complementary role by aligning portfolio structure with retirement objectives. As individuals move closer to retirement, investment priorities often shift from growth toward income stability and risk management. Coordinating these shifts within a broader investment framework supports smoother transitions and reduces unintended consequences.

For business owners, retirement planning in Canada must also align with business strategy. Business value, succession planning, and exit timing all influence retirement outcomes. Integrating retirement planning with business-focused financial strategy ensures that long-term goals remain achievable even as professional responsibilities evolve.

A coordinated approach that integrates retirement strategy with long-term investment planning and broader financial goals creates a cohesive plan that adapts over time rather than relying on static projections.

Building a Clear and Sustainable Retirement Plan

A successful retirement plan is not defined by a single number or milestone. It is defined by clarity, flexibility, and the ability to adapt as life and financial conditions change. Canadians who approach retirement planning with structure and foresight are better positioned to maintain confidence throughout retirement.

Clarity comes from understanding income sources, spending needs, and long-term risks. When these elements are clearly defined, financial decisions become more deliberate and less reactive. This clarity reduces uncertainty and supports consistent decision-making over time.

Flexibility is equally important. Retirement plans must accommodate changing markets, health considerations, and personal priorities. A well-designed plan anticipates uncertainty and includes mechanisms for adjustment without compromising long-term sustainability.

Sustainability is achieved through coordination. When income planning, investment strategy, and tax considerations work together, retirement resources are more likely to last. This coordination is at the heart of structured retirement planning and distinguishes comprehensive strategies from ad hoc solutions.

For individuals seeking clarity and confidence in their retirement strategy, working within a structured framework supported by dedicated retirement planning services can help transform long-term uncertainty into a manageable and well-defined plan.

retirement planning in Canada retirement planning in Canada retirement planning in Canada retirement planning in Canada

Bringing It All Together: Creating a Retirement Plan That Works in Canada

A well-structured retirement plan brings together every financial decision into a cohesive strategy. Rather than treating savings, investments, and government benefits as separate elements, effective retirement planning aligns them to support long-term income stability and peace of mind. This alignment is what transforms fragmented decisions into a clear, sustainable plan.

Clarity is one of the most valuable outcomes of retirement planning in Canada. When individuals understand where their income will come from, how long it is expected to last, and how different choices affect future flexibility, financial decisions become more deliberate. This clarity reduces the anxiety that often accompanies major life transitions and supports more confident decision-making.

Consistency also plays a critical role. Retirement planning is not about predicting the future with certainty, but about building a framework that can adapt to change. Markets fluctuate, tax rules evolve, and personal circumstances shift over time. A robust retirement plan anticipates these changes and allows for adjustments without undermining long-term goals.

Another defining feature of successful retirement planning is coordination. Income planning, investment structure, and tax efficiency must work together rather than in isolation. When these elements are coordinated, retirees are better positioned to preserve purchasing power, manage risk, and maintain flexibility throughout retirement.

For many Canadians, moving from uncertainty to confidence requires structured guidance. A comprehensive approach supported by ongoing retirement planning supporthelps ensure that strategies remain aligned as financial and personal circumstances evolve.

At Sentra Financial Group, we believe financial success isn’t about luck — it’s about strategy, discipline, and trust. Our mission is to help individuals and families achieve peace of mind through smart investing, life insurance, and long-term financial planning.

Frequently Asked Questions About Retirement Planning in Canada

What is the main goal of retirement planning in Canada?

The primary goal of retirement planning is to ensure sustainable income throughout retirement while managing risk and taxes effectively. Rather than focusing solely on how much money is saved, retirement planning emphasizes how income is generated, coordinated, and maintained over time. This approach supports long-term financial stability and lifestyle continuity.

How much money do I need to retire comfortably in Canada?

There is no single number that applies to everyone. Retirement needs depend on lifestyle expectations, location, health considerations, and income sources such as pensions and government benefits. Retirement planning helps translate personal goals into realistic income targets rather than relying on generalized estimates.

When should Canadians start retirement planning?

Ideally, retirement planning should begin well before retirement is imminent, as earlier planning provides greater flexibility. However, starting later can still lead to meaningful improvements through better withdrawal strategies, tax coordination, and income planning. What matters most is adopting a structured approach as soon as financial decisions begin to affect long-term outcomes.

How do CPP and OAS fit into a retirement plan?

CPP and OAS provide foundational income for many retirees, but the timing of these benefits has a significant impact on long-term results. Retirement planning evaluates when to begin these benefits in coordination with personal savings and pensions to support income stability and tax efficiency over time.

Is retirement planning only important for high-income individuals?

No. Retirement planning is valuable for individuals across income levels. While higher-income households may face greater complexity, anyone who wants predictable income, reduced tax exposure, and long-term clarity can benefit from structured retirement planning.