As we enter 2026, Canadian retirees face a significantly more complex financial landscape than previous generations. With inflation impacting purchasing power and tax brackets shifting, the question is no longer just “how much have I saved?” but rather “how much can I keep after taxes?” The two primary vehicles for this wealth—the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA) (RRSP vs TFSA)—require completely different tactical approaches when it comes time to turn those savings into a steady paycheck.

Many Canadians spend decades diligently contributing to these accounts without a clear exit strategy. However, the withdrawal phase, often called the “decumulation” phase, is where the most significant tax mistakes occur. A poorly timed withdrawal from an RRSP can trigger a massive tax bill or cause a clawback of your Old Age Security (OAS) benefits. This is why Personal Financial Planning in Canada must focus heavily on the sequence and timing of these distributions.

In 2026, the stakes are even higher due to the increased cost of living in major hubs like Toronto. Every dollar saved in taxes is a dollar that can be reinvested or spent on your lifestyle. As we’ve explored in our guide on Wealth Management in Canada, protecting your capital from unnecessary erosion is the cornerstone of long-term financial health. This article will provide a definitive roadmap for balancing your RRSP and TFSA withdrawals.

Strategic withdrawal planning is not a “one-size-fits-all” process. It depends on your current tax bracket, your expected longevity, and your estate planning goals. For some, emptying the RRSP early makes sense; for others, the TFSA should be the last line of defense. By understanding the interaction between these accounts and government pensions like the CPP, which we detailed in our Retirement Planning in Canada guide, you can create a tax-efficient income stream that lasts a lifetime.

Ultimately, the goal of this guide is to empower you to make informed decisions that align with the 2026 tax realities. Whether you are working with a Financial Planner and Retirement Specialist or managing your own portfolio, these strategies will help you navigate the complexities of the Canada Revenue Agency (CRA) rules while keeping more of your hard-earned money in your pocket.

Table of Contents

The Core Mechanics of RRSP vs TFSA in 2026

To master the withdrawal phase, one must first understand the fundamental “DNA” of these two accounts. While both are registered with the CRA, they offer opposite tax advantages. The RRSP is a “Tax-Deferred” account, meaning you get a break now but pay later. The TFSA is a “Tax-Free” account, meaning you pay the tax upfront (by using after-tax dollars to contribute) but never pay a cent to the CRA on that money ever again.

RRSP: The Power of Tax Deferral

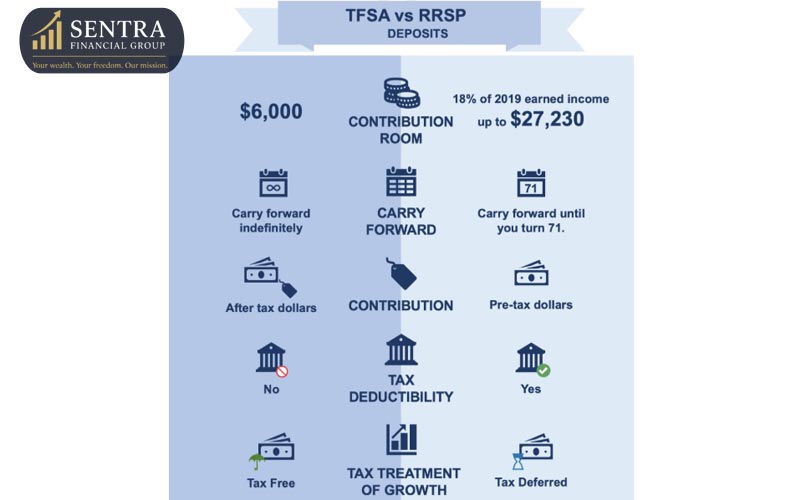

The RRSP has been the traditional go-to for Canadian retirement for decades. In 2026, the maximum contribution limit has risen to $33,810 (or 18% of your previous year’s earned income). The primary allure is the immediate tax deduction. If you are in a high tax bracket today, every dollar you contribute reduces your taxable income, often resulting in a significant tax refund.

However, the “catch” with the RRSP is that the government is essentially your business partner. Every dollar you withdraw in retirement is added to your income and taxed at your marginal rate. This is why many retirees are shocked to see 30% or 40% of their withdrawal disappear into taxes. Proper Investment Planning in Canada involves projecting what your future tax bracket will be to ensure the RRSP is actually providing a net benefit.

TFSA: The Flexibility of Tax-Free Growth

The TFSA is arguably the most flexible tool in the Canadian financial toolkit. For 2026, the annual contribution limit is $7,000. If you have been eligible since its inception in 2009 and have never contributed, your total available room now sits at a substantial $109,000. Unlike the RRSP, your contributions are made with money you have already paid tax on, so the CRA has no claim on the growth or the withdrawals.

The magic of the TFSA in retirement lies in its “invisibility.” Withdrawals do not count as income. This means they do not affect your eligibility for income-tested benefits like the Guaranteed Income Supplement (GIS) or trigger the OAS clawback. For business owners, the TFSA is an essential part of Financial Planning for Business Owners, providing a source of liquidity that doesn’t complicate corporate tax filings or personal income thresholds.

Withdrawal Sequence: Which Account Should You Empty First?

The order in which you withdraw from your accounts can make a difference of hundreds of thousands of dollars over a 30-year retirement. In 2026, the traditional advice of “spend your non-registered money first, then your RRSP, and finally your TFSA” is being challenged by new tax realities. A smarter sequence often involves a “blended” approach to keep you in the lowest possible tax bracket throughout your life.

If you have a very large RRSP, it might be beneficial to start small withdrawals in your early 60s, even if you don’t need the money. This “meltdown” strategy prevents you from being pushed into a massive tax bracket at age 72 when RRIF minimums become mandatory. By using these early RRSP withdrawals to fund your lifestyle, you can allow your TFSA to continue growing tax-free for as long as possible. As highlighted in our Retirement Planning in Toronto case studies, this can prevent “tax spikes” in later years.

Conversely, if you expect your income to be higher in the future (perhaps due to an inheritance or the sale of a business), it is better to prioritize RRSP withdrawals now while your bracket is low. The goal is “Tax Bracket Management”—aiming to have a consistent taxable income level every year rather than having $40,000 one year and $120,000 the next.

Pro-Rata vs. Sequential Withdrawals

Many of our clients in Wealth Management in Canada find success with a pro-rata approach. This involves taking a portion of your income from taxable sources (RRSP/RRIF) and a portion from tax-free sources (TFSA). For example, taking $40,000 from an RRSP and $20,000 from a TFSA results in $60,000 of cash flow, but only $40,000 of taxable income. This often keeps the individual below the next federal tax threshold, which in 2026 is a significant saving.

Managing the RRIF Conversion at Age 71

By December 31st of the year you turn 71, the CRA mandates that you close your RRSP. Most Canadians choose to convert it into a Registered Retirement Income Fund (RRIF). Once converted, you are no longer allowed to put money in; you must take a minimum amount out every year based on your age.

In 2026, the minimum withdrawal rates remain a concern for many. At age 72, the minimum is 5.40%, and it scales up every year. If your RRSP is significant—say $1 million—your mandatory withdrawal at 72 would be $54,000. When added to your CPP and OAS, this can easily trigger the OAS clawback. This is why Investment Planning in Canada must include a “pre-71” plan to reduce the RRSP balance strategically before the mandatory RRIF rules take over.

Furthermore, you can choose to base your RRIF minimum on your spouse’s age if they are younger. This allows for a lower mandatory withdrawal, keeping more money in the tax-deferred environment for longer. This is a common tactic we discuss during Financial Planning for Business Owners, as it provides more control over personal taxable income.

Impact on Government Benefits (OAS and GIS)

One of the most overlooked aspects of a withdrawal strategy is how a simple RRSP withdrawal can create a “hidden tax” by reducing your government benefits. In 2026, the CRA and Service Canada look at your Net Income to determine your eligibility for the Guaranteed Income Supplement (GIS) and to calculate the Old Age Security (OAS) Recovery Tax.

For low-to-moderate-income retirees, every dollar taken from an RRSP is considered income and can reduce GIS payments by as much as 50 cents on the dollar. This creates a staggering effective tax rate. In contrast, withdrawing from a TFSA has zero impact on these benefits. This is why Personal Financial Planning in Canada must be surgical; if you are eligible for GIS, it is often better to exhaust TFSA funds first to keep your reported income as low as possible.

For higher earners, the OAS Clawback (which we analyzed in our previous guide on Retirement Planning in Canada) remains the primary concern. Since the 2026 threshold is approximately $95,323, a large RRIF withdrawal can easily push you over this limit. By strategically using TFSA withdrawals to supplement your lifestyle, you can keep your “reported” income just below the clawback threshold, effectively saving yourself a 15% surcharge on your OAS pension.

The “Meltdown” Strategy: Withdrawing RRSPs Early

The “RRSP Meltdown” is a sophisticated strategy often used in Wealth Management in Canada to reduce the total tax liability over a lifetime. The core idea is to begin withdrawing from your RRSP in your early 60s—before you are forced to do so at age 72—even if you don’t immediately need the cash for living expenses.

Why Meltdown Your RRSP?

The goal is to “smooth out” your tax brackets. If you leave your RRSP untouched until age 72, you may find yourself forced to take large RRIF minimums that put you in a 40% or 50% tax bracket. By taking smaller, controlled amounts between ages 60 and 71, you might only pay 20% or 25% tax. The “melted” funds can then be moved into a TFSA (if room is available) or a non-registered account, where they grow more tax-efficiently.

The Multi-Generational Benefit

An RRSP meltdown is also an excellent estate planning tool. Upon the death of the second spouse, the entire remaining RRSP/RRIF balance is treated as income in a single year, which often results in the top tax bracket (over 50% in Ontario). By melting down the account while you are alive, you are effectively paying a lower tax rate now so that your heirs receive a larger, tax-paid inheritance. This is a key discussion point for our clients looking at Investment Planning in Canada.

Income Splitting Strategies for Couples

In 2026, Canadian tax laws continue to offer a powerful advantage for couples: Pension Income Splitting. If one partner has a significantly larger RRSP/RRIF than the other, they can potentially allocate up to 50% of that income to their spouse for tax purposes.

This is particularly effective when one spouse is in a high tax bracket and the other is in a lower one. By shifting the income, you utilize the lower earner’s basic personal amount and lower tax tiers. This strategy also applies to life annuities and, in some cases, CPP (through pension sharing).

For Business Owners in Canada, income splitting becomes even more vital. If you have been paying yourself a salary to build an RRSP, using the RRIF conversion as a tool to split income with a spouse who was perhaps a lower-income earner in the business can drastically reduce the household’s total tax bill in retirement. It’s a prime example of how professional Wealth Management in Canada adds value beyond simple stock picking.

2026 Contribution Limits and Deadlines

Even as you begin the withdrawal phase, it is crucial to stay aware of the contribution limits, as you may still be earning income or wanting to shift assets.

- RRSP Limit 2026: $33,810 (based on 18% of 2025 earned income).

- TFSA Limit 2026: $7,000 (bringing the total cumulative room for a lifelong eligible resident to $109,000).

- RRSP Deadline: The first 60 days of 2027 for the 2026 tax year.

Remember, if you are over 71, you can no longer contribute to your own RRSP, but you can contribute to a Spousal RRSP if your spouse is 71 or younger and you still have “earned income” room. This is a subtle but effective way to continue reducing your tax bill even in your 70s.

Frequently Asked Questions (FAQs)

As we navigate the fiscal landscape of 2026, many Canadians have specific questions about the practical application of their withdrawal strategies. Here are the most common inquiries our specialists receive:

Can I put money back into my RRSP after I’ve withdrawn it?

Unlike the TFSA, RRSP contribution room is “one and done.” Once you withdraw funds from an RRSP, you do not get that contribution room back (unless you are using the Home Buyers’ Plan or Lifelong Learning Plan). This is why we often suggest exploring Investment Strategies for the Affluent before tapping into your RRSP for liquidity.

What is the TFSA contribution limit for 2026?

The annual TFSA contribution limit for 2026 is $7,000. If you have been eligible since 2009 and have never contributed, your total cumulative room is now $109,000. This makes the TFSA a massive secondary pillar for tax-free retirement income.

Should I withdraw from my TFSA or RRSP for an emergency?

Generally, the TFSA is the better choice for emergencies. Withdrawals are tax-free, and you get the contribution room back on January 1st of the following year. RRSP withdrawals, however, trigger immediate withholding tax and permanent loss of room.

How does the CRA calculate the withholding tax on RRSP withdrawals? In 2026 (outside of Quebec), the rates are:

-10% for amounts up to $5,000.

-20% for amounts between $5,001 and $15,000.

-30% for amounts over $15,000. Remember, this is just a “pre-payment” of your tax; the final amount you owe depends on your total annual income.

Is it better to use a Spousal RRSP even if we are both in the same tax bracket?

Yes, because it provides more flexibility for future Wealth Management in Canada. It allows for strategic income splitting before you reach age 65, which is when the general pension income-splitting rules typically begin to apply to RRIF income.

Conclusion: Customizing Your Withdrawal Roadmap

Designing the perfect withdrawal sequence is the ultimate “stress test” for any financial plan. In 2026, the intersection of inflation, shifting tax brackets, and government benefit thresholds makes it impossible to rely on old, static advice. Whether you prioritize a “meltdown” of your RRSP to protect your estate or keep your TFSA as a tax-free legacy for your heirs, your strategy must be as dynamic as the economy.

Successful Retirement Planning in Canada is not about following a single rule, but about finding the right “mix” for your unique situation. For business owners, this might mean balancing corporate dividends with RRIF minimums. For families in Toronto, it might mean using the TFSA to bridge the gap until CPP and OAS kick in.

At Sentra Financial Group, we specialize in helping Canadians navigate these high-stakes decisions. By integrating Investment Planning in Canada with deep tax-efficiency expertise, we ensure that you don’t just reach retirement—you thrive in it. Your hard-earned savings deserve a plan that works as hard as you did to earn them.

At Sentra Financial Group, we believe financial success isn’t about luck — it’s about strategy, discipline, and trust. Our mission is to help individuals and families achieve peace of mind through smart investing, life insurance, and long-term financial planning.