Wealth management in Canada is not simply about accumulating assets or accessing sophisticated investment products. It is a structured approach to coordinating financial decisions in a way that protects capital, manages risk, and supports long-term personal and family goals. As financial situations grow more complex, the need for a comprehensive wealth management strategy becomes increasingly important.

Many Canadians assume wealth management is only relevant at very high levels of net worth. In reality, wealth management in Canada becomes essential whenever multiple financial elements must work together. Investments, taxes, income planning, and long-term objectives all interact in ways that require coordination rather than isolated decision-making.

Without a structured wealth management approach, financial decisions are often made independently. Investment portfolios may grow, but tax efficiency, risk exposure, and long-term sustainability remain misaligned. Over time, this lack of coordination can erode real wealth and increase uncertainty, even for individuals with significant assets.

Wealth management in Canada focuses on aligning financial strategy with purpose. Rather than reacting to markets or short-term opportunities, it emphasizes discipline, structure, and long-term clarity. This approach helps individuals maintain control over their financial lives across changing market and personal conditions.

At its core, wealth management in Canada integrates investing, tax planning, risk management, and long-term planning into a cohesive framework. When these elements work together, wealth becomes a tool that supports stability, flexibility, and confidence rather than a source of complexity.

Table of Contents

What Is Wealth Management in Canada?

Wealth management in Canada refers to a comprehensive process of managing financial resources through coordinated strategy rather than isolated actions. It goes beyond basic investing by considering how assets, income, taxes, and long-term goals interact over time.

Unlike standalone investment management, wealth management in Canada takes a holistic view of an individual’s financial situation. Decisions are evaluated based on their impact across the entire financial landscape, including retirement readiness, tax exposure, and long-term sustainability.

One defining characteristic of wealth management in Canada is integration. As assets grow, financial decisions become increasingly interconnected. Investment choices influence tax outcomes, income planning affects portfolio structure, and risk management shapes long-term resilience. Wealth management addresses this complexity by aligning decisions within a single strategic framework.

Time horizon plays a central role in wealth management. Strategies are designed to function across decades, not just market cycles. This long-term perspective helps individuals navigate volatility while maintaining focus on enduring objectives rather than short-term results.

Wealth management builds on the foundation established through personal financial planning in Canada, extending that structure to address higher levels of coordination, responsibility, and long-term impact.

Why Wealth Management Matters in the Canadian Financial System

The Canadian financial environment presents unique challenges that make wealth management especially relevant. Progressive taxation, diverse investment vehicles, and evolving regulatory frameworks require careful coordination to preserve and grow wealth effectively.

Tax efficiency is one of the most significant factors influencing long-term outcomes. As assets increase, taxes can become one of the largest drags on wealth. Wealth management in Canada focuses on structuring income, investments, and asset ownership to improve after-tax results rather than concentrating solely on pre-tax growth.

Market volatility also underscores the importance of structured wealth management. Larger portfolios are often more exposed to market fluctuations, making disciplined risk management essential. Wealth management strategies aim to balance growth and preservation, reducing the likelihood that volatility undermines long-term plans.

Complexity is another key consideration. Multiple accounts, investment strategies, and income sources can make financial oversight challenging. Wealth management in Canada provides a centralized framework that simplifies decision-making while maintaining strategic control.

In addition, wealth management supports long-term planning beyond individual outcomes. Family considerations, legacy goals, and future transitions all benefit from a coordinated approach that aligns wealth with broader life objectives.

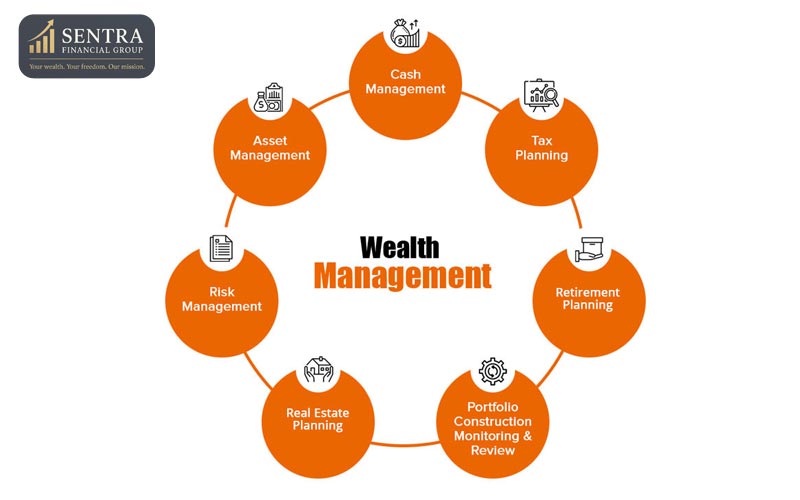

Core Components of Wealth Management in Canada

Effective wealth management in Canada is built on several interconnected components that must function together to support long-term stability. Each component plays a distinct role while reinforcing the overall strategy.

Investment coordination is a central element. Rather than managing investments in isolation, wealth management aligns portfolio structure with tax considerations, income needs, and long-term goals. This coordination helps ensure that investment decisions support broader financial objectives.

Tax planning is another critical component. As financial complexity increases, proactive tax management becomes essential. Wealth management in Canada emphasizes planning ahead to preserve capital and improve efficiency rather than reacting to tax liabilities after they occur.

Risk management also plays a vital role. Protecting wealth requires identifying and mitigating risks that could disrupt long-term plans, including market risk, concentration risk, and unexpected life events. A comprehensive approach balances opportunity with resilience.

Strategic oversight ties these components together. Wealth management in Canada involves ongoing review and adjustment to ensure strategies remain aligned as circumstances evolve. This continuous oversight distinguishes wealth management from static financial planning.

Wealth Management vs Investment Management

Wealth management in Canada is often confused with investment management, but the two are not interchangeable. Investment management focuses primarily on portfolio construction and performance, whereas wealth management takes a broader view by coordinating investments with taxes, income planning, risk management, and long-term objectives. This distinction becomes increasingly important as financial complexity grows.

Investment management answers the question of how assets are invested, while wealth management in Canada addresses why those investments exist and how they support a wider financial strategy. Without this broader context, even well-performing portfolios can fall short of delivering long-term stability or flexibility.

Another key difference lies in scope. Investment management typically operates within the boundaries of a single account or portfolio. Wealth management, by contrast, evaluates how multiple accounts, income sources, and ownership structures interact. This integrated approach helps prevent inefficiencies that arise when decisions are made in silos.

Time horizon further separates the two. Investment management often emphasizes shorter evaluation periods based on performance benchmarks. Wealth management in Canada is inherently long-term, focusing on sustainability across decades and through multiple life stages, including transitions such as retirement or business exit.

Ultimately, investment management is a component of wealth management rather than a substitute for it. When integrated within a comprehensive framework that also incorporates investment planning considerations, wealth management provides a more resilient and purpose-driven approach to long-term financial decision-making.

Tax-Efficient Wealth Structuring in Canada

Tax efficiency is one of the most critical pillars of wealth management in Canada. As wealth grows, the impact of taxes becomes more pronounced, often representing one of the largest constraints on long-term outcomes. Proactive tax-aware structuring helps preserve capital and improve after-tax results over time.

Wealth management in Canada emphasizes the strategic use of registered and non-registered accounts to manage tax exposure. Placing the right assets in the right accounts can significantly influence long-term efficiency. Without coordination, individuals may inadvertently increase taxes even when investment performance is strong.

Income structuring also plays a major role. Different forms of income are taxed differently, and the timing of income recognition can affect marginal tax rates and benefit eligibility. Wealth management strategies aim to smooth income over time and reduce unnecessary tax spikes.

Ownership structure is another important consideration. How assets are held—personally, jointly, or through corporate structures—can affect tax outcomes and flexibility. Wealth management in Canada evaluates these structures in the context of long-term goals rather than short-term convenience.

Tax-efficient structuring works best when integrated with broader financial planning. Coordinating tax strategy with personal financial planning in Canada ensures that tax efficiency supports overall objectives rather than operating in isolation.

Wealth Management Across Life Stages

Wealth management in Canada evolves as individuals move through different phases of life. Financial priorities, risk tolerance, and planning horizons change over time, requiring strategies that adapt while maintaining long-term alignment.

Early stages often focus on building foundational wealth and establishing disciplined habits. Wealth management at this stage emphasizes growth-oriented strategies while laying the groundwork for future complexity. Decisions made early can have a disproportionate impact due to the influence of time.

Mid-life introduces greater complexity. Career advancement, family responsibilities, and increased assets require more coordinated planning. Wealth management in Canada during this phase focuses on balancing growth with protection while preparing for future transitions such as retirement.

Later stages shift emphasis toward preservation and income sustainability. As individuals approach or enter retirement, wealth management strategies are refined to support predictable income, manage risk, and maintain flexibility. This stage often overlaps closely with retirement planning considerations.

Across all stages, wealth management provides continuity. By maintaining a structured framework, individuals can navigate change without losing sight of long-term objectives, ensuring that wealth continues to support evolving needs and priorities.

Common Wealth Management Challenges in Canada

Even with significant assets, Canadians often face challenges that complicate wealth management. One common issue is fragmentation. Managing accounts, investments, and strategies independently can lead to inefficiencies and increased risk, undermining long-term outcomes.

Another challenge is overexposure to specific risks. Concentration in a single investment, sector, or income source can create vulnerability. Wealth management in Canada addresses this by promoting diversification and balanced risk management.

Tax inefficiency is also a frequent concern. Without coordinated planning, taxes can erode wealth over time. Wealth management strategies aim to anticipate tax consequences rather than reacting to them after the fact.

Behavioral factors further complicate wealth management. Emotional responses to market volatility or life events can lead to inconsistent decision-making. A structured approach helps maintain discipline and long-term focus.

Addressing these challenges requires ongoing oversight and coordination. Wealth management in Canada provides a framework for identifying risks early and implementing adjustments that preserve long-term stability.

Integrating Wealth Management With Broader Financial Strategy

Wealth management in Canada is most effective when integrated with a broader financial strategy rather than treated as a standalone service. Investments, tax planning, and risk management must align with overall financial objectives to support long-term success.

Personal financial planning provides the foundation upon which wealth management is built. Cash flow management, goal setting, and risk tolerance established earlier in life shape how wealth strategies are designed and implemented. Integrating wealth management with broader financial planning ensures coherence and direction.

For individuals with business interests, integration becomes even more important. Business value, income timing, and succession planning all influence personal wealth outcomes. Coordinating wealth management with business-focused financial planning helps reduce reliance on a single outcome and supports diversification.

Integration also supports adaptability. When wealth management operates within a unified framework, adjustments can be made thoughtfully as circumstances change without disrupting overall strategy.

Ultimately, integrated wealth management transforms complexity into clarity. By aligning decisions across financial domains, wealth becomes a resource that supports long-term confidence and stability.

The Role of Wealth Management in Long-Term Decision-Making

Wealth management in Canada plays a critical role in shaping long-term financial decision-making. As financial lives become more complex, decisions made today often have consequences that extend decades into the future. Without a structured framework, it becomes difficult to evaluate trade-offs or understand how individual choices affect long-term outcomes.

One of the key contributions of wealth management is providing context. Rather than evaluating decisions in isolation, wealth management in Canada considers how choices related to investing, taxation, and asset ownership interact over time. This broader perspective helps individuals avoid short-term decisions that may undermine long-term objectives.

Wealth management also supports consistency in decision-making. Financial markets, economic conditions, and personal circumstances inevitably change, but long-term goals tend to remain relatively stable. A wealth management framework helps individuals stay aligned with those goals even when external conditions create pressure to deviate.

Another important aspect is prioritization. As wealth grows, opportunities and choices multiply, making it harder to determine where attention and resources should be focused. Wealth management in Canada helps clarify priorities, ensuring that time, capital, and risk are allocated in a way that supports what matters most over the long term.

Ultimately, wealth management transforms decision-making from a reactive process into a strategic one. By aligning daily financial choices with long-term vision, wealth management in Canada helps individuals maintain clarity, confidence, and control throughout changing life stages.

Conclusion: A Structured Approach to Wealth Management in Canada

Wealth management in Canada is ultimately about structure, coordination, and long-term clarity. As financial situations become more complex, isolated decisions around investing, taxes, or risk management are rarely sufficient to support sustainable outcomes. A comprehensive wealth management approach brings these elements together within a single strategic framework.

One of the defining advantages of wealth management is its ability to transform complexity into coherence. By aligning investments with tax efficiency, income planning, and long-term objectives, individuals gain greater control over their financial future. This alignment reduces uncertainty and supports more consistent decision-making over time.

Wealth management in Canada also emphasizes adaptability. Markets fluctuate, tax rules evolve, and personal circumstances change. A structured approach allows strategies to be reviewed and refined without losing sight of overarching goals. This balance between stability and flexibility is essential for long-term success.

Another key benefit of wealth management is risk awareness. Rather than reacting to challenges after they arise, proactive planning helps identify vulnerabilities early and address them thoughtfully. This forward-looking perspective protects not only financial capital but also long-term peace of mind.

For Canadians seeking clarity, control, and sustainability in their financial lives, wealth management in Canada provides a disciplined approach that aligns resources with purpose and supports confidence across every stage of life.

At Sentra Financial Group, we believe financial success isn’t about luck — it’s about strategy, discipline, and trust. Our mission is to help individuals and families achieve peace of mind through smart investing, life insurance, and long-term financial planning.

FAQ About Wealth Management in Canada

What is wealth management in Canada?

Wealth management in Canada is a comprehensive approach to managing financial resources that integrates investing, tax planning, risk management, and long-term financial strategy. It focuses on coordination rather than isolated financial decisions.

How is wealth management different from financial planning?

Financial planning establishes goals, priorities, and structure, while wealth management builds on that foundation to manage greater complexity. Wealth management in Canada typically involves deeper coordination of investments, taxes, and long-term strategy as assets grow.

Is wealth management only for high-net-worth individuals?

Not necessarily. Wealth management in Canada becomes valuable whenever financial complexity increases, such as having multiple accounts, diverse income sources, business interests, or long-term planning needs.

Why is tax efficiency so important in wealth management?

Tax efficiency directly affects after-tax outcomes, which ultimately determine real wealth growth. Wealth management in Canada focuses on coordinating account types, income timing, and asset ownership to reduce unnecessary tax exposure over time.

How does wealth management support retirement planning?

Wealth management supports retirement planning by aligning investments, tax strategy, and risk management to help create sustainable retirement income. It ensures that long-term retirement goals are integrated into broader financial strategy.

Is wealth management a one-time service?

No. Wealth management in Canada is most effective as an ongoing process. Regular review and adjustment help ensure strategies remain aligned with changing markets, regulations, and personal circumstances.

When should someone consider professional wealth management?

Professional wealth management may be appropriate when financial decisions become more complex or when long-term coordination across multiple areas is needed. It provides structure, objectivity, and accountability as financial situations evolve.